Money plays an important role in life. It supports our decisions, our lifestyle, our freedom, and ultimately our ability to live the kind of life we want.

But having money alone does not automatically create security or clarity. Having savings, or even having investments, does not necessarily mean a person is truly prepared for the future.

This becomes especially important when we talk about retirement, one of the most significant financial stages in life. At some point, whether by choice or circumstance, income from work may decrease or stop completely. When that happens, financial life shifts from the phase of earning income to the phase of depending on what has already been accumulated.

That transition is when many people realize that saving alone may not be enough. The important question is not only how much money you have, but whether there is a clear financial structure behind that money.

A financial plan is not just something nice to have. For many people, it is a necessary foundation for preparing for the financial future of themselves and their families.

Retirement is not a question of “if,” but “when”

Many people rarely stop to ask themselves: if one day I no longer work, what will my life look like?

In reality, the more accurate question is not “if,” but “when.” At some point, most people will have to slow down or stop working. It may be because of health, age, family responsibilities, or simply because they no longer want to continue exchanging their time for income in the same way.

At that point, the question is no longer how much money you earn each month. The question becomes how much you have prepared for the stage when employment income is no longer the main source of support.

This is where many people begin to notice a major problem. They may have saved for years, but they do not truly know where they are going. They have money, but they do not have a clear plan behind that money.

Retirement is not a random event. It is a goal. And like any important goal in life, without a plan, it remains only an idea.

You cannot build a strong house without a blueprint. In the same way, it is difficult to build long-term financial stability without a clear structure.

Saving money is the first step, but saving alone does not answer the most important question: do you have enough to retire?

Without a plan, you may not know how much is enough, whether you are moving too slowly or too quickly, or whether you are even moving in the right direction. A financial plan helps turn those unclear questions into something more specific, measurable, and easier to understand.

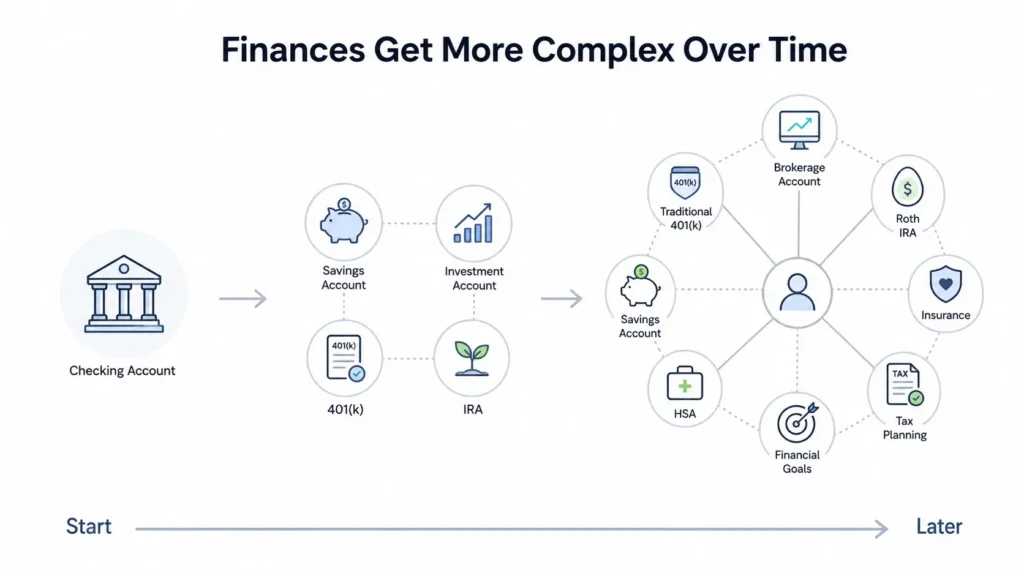

Personal finances often become more complex over time

When someone first starts working, personal finance may feel simple. There may only be one bank account for receiving income, paying expenses, and saving money.

But over time, financial life usually becomes more complicated. A person may open savings accounts, investment accounts, and accounts at different brokerage firms or financial platforms. As their career becomes more established, they may also have a 401(k), IRA, Roth IRA, life insurance, health insurance, and other financial tools.

At some point, they may look back and realize they have many accounts, many products, and many different financial pieces. But the problem is that they may not fully understand how all of those pieces work together.

Each financial tool has its own role. But those tools do not automatically coordinate with one another. Each account may have its own tax rules, contribution limits, withdrawal rules, and consequences if it is used at the wrong time or in the wrong way.

Without understanding these details, it becomes easy to make decisions that are not optimal. For example, someone may withdraw money at the wrong time, invest too aggressively or too conservatively, miss potential tax advantages, or keep many accounts without a clear overall strategy.

Over time, this complexity usually does not decrease. It increases. Without a comprehensive financial plan, a person may end up having “many things” but not knowing exactly what purpose those things are serving.

A financial plan does not make life more complicated. Instead, it provides a system for organizing the different parts of your financial life so they can work together toward a clearer direction.

It is not only about how much money you have, but how long that money can support you

One important question many people have not clearly answered is this: if you stopped working today, how long could your money support you?

The question is not only how much money is in your accounts. It is whether that money can sustain your lifestyle for 5 years, 10 years, 20 years, or 30 years.

This becomes even more important when you begin thinking more deeply about life after retirement. What kind of lifestyle do you want? Do you want to travel once a year, twice a year, or more often? Do you want to stay in one place, relocate, help your children or grandchildren, support family members, or leave assets for the next generation?

These may sound like personal preferences, but they are also financial questions.

Retirement is not simply about reaching a certain number in an account. Retirement is about the ability to maintain a lifestyle over a long period of time.

Without a plan, you are often guessing. And when people guess, they usually fall into one of two situations. Either they spend too much and face the risk of running out of money too early, or they become overly cautious, spend too little, and never fully enjoy life even after many years of saving and investing.

A financial plan helps answer these questions with more concrete numbers. It can help estimate spending needs, income sources, withdrawal strategies, the sustainability of assets, and the risks that may affect life after retirement.

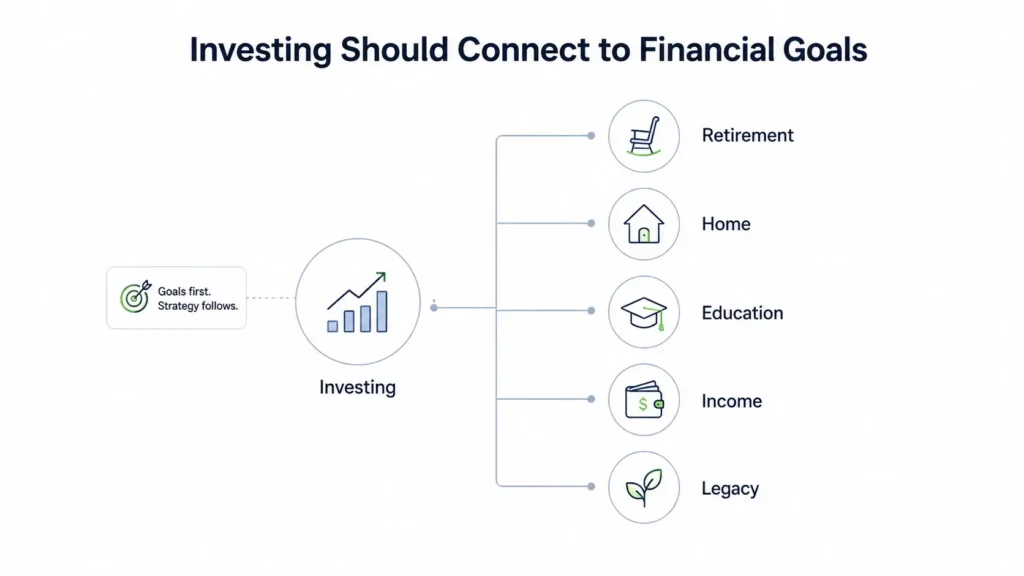

Investing should be connected to financial goals

Many people think investing is simply about choosing good stocks, selecting good funds, or finding the right time to buy and sell. But in reality, investing only becomes truly meaningful when it is connected to a clear financial plan.

If you do not know what your goal is, it is difficult to know how you should invest.

A 30-year-old who is investing for the next 30 years will have very different needs from a 60-year-old who is preparing to retire in the next few years. A person with stable income, low expenses, and few family responsibilities will have a different situation from someone who is raising children, paying debt, supporting parents, and preparing for future healthcare costs.

That is why the question is not only “Where should I invest?” The better question is: “Does this investment strategy fit my life, my goals, and my risk tolerance?”

A financial plan helps connect the investment portfolio to real-life goals. It helps answer questions such as: how much growth do I need, how much volatility can I tolerate, when will I need this money, and which accounts should be used for short-term, long-term, or retirement goals?

Without a plan, investing can easily become a series of disconnected decisions. A little money goes into one account, a little into another account, another decision comes from something someone heard online, and emotional reactions may take over when the market becomes volatile.

But when there is a plan, investing becomes part of a broader strategy. Each decision has a clearer reason behind it and is connected to a long-term objective.

Taxes, withdrawal timing, and asset allocation can make a meaningful difference

In personal finance, major mistakes do not always come from one obvious bad decision. Many times, they come from small inefficiencies that repeat over time.

A tax decision that was not well planned. A withdrawal made at the wrong time. An investment portfolio that does not fit the current stage of life. An account used for the wrong purpose. Each of these decisions may not seem dramatic on its own, but over time, the cost can become significant.

For example, a 4% difference on a $500,000 account equals $20,000. And that is only one factor. When you add possible mistakes related to taxes, withdrawal timing, investment allocation, or account coordination, the total cost can become much larger.

For most people, the issue is not that they are not intelligent. The issue is that personal finance, especially when it involves retirement, taxes, investing, and long-term assets, can become too complex to manage accurately without structure.

A financial plan helps bring these factors into a clearer system. It helps compare options, evaluate consequences, and make more thoughtful decisions over time.

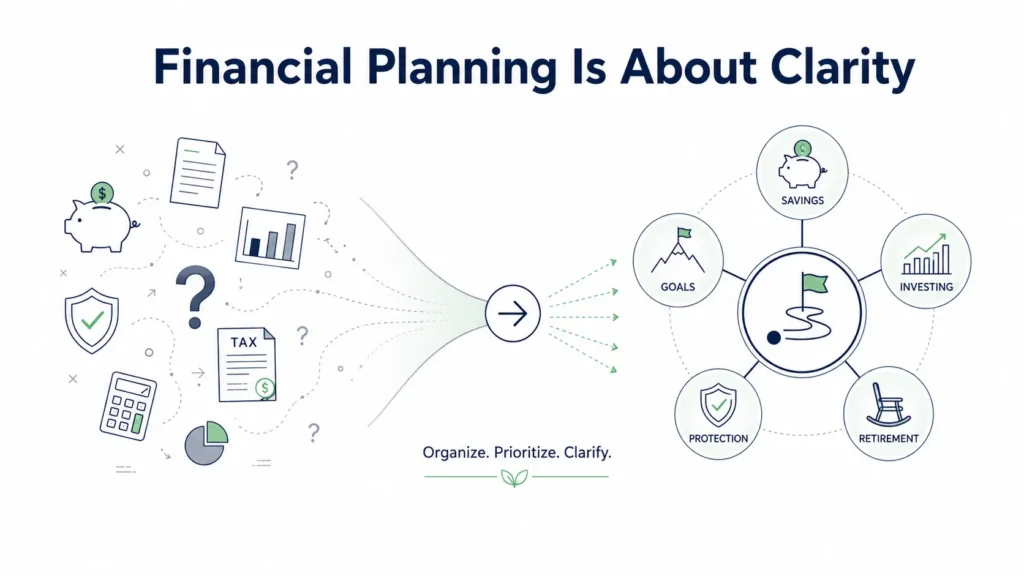

Financial planning is not about complexity. It is about clarity.

A financial plan is not meant to make financial life more complicated. Its purpose is to create clarity.

It helps you understand where you are today, what you want your future life to look like, and what path may help you move from your current position toward that future.

Without a plan, financial decisions often become disconnected. Save a little, invest a little, buy some insurance, open another account, but without a clear connection between all of those pieces.

Over time, that lack of connection creates uncertainty.

But with a specific plan, the pieces begin to work together: income, spending, saving, investing, taxes, insurance, retirement, and long-term goals. Each decision has a reason, and each part serves a broader purpose.

That is the difference between simply having money and understanding how to use money.

Retirement should not be something people only start thinking about when they are close to leaving work. It should not be something they simply hope will work out when the time comes. Retirement is a stage of life that should be intentionally designed, step by step, over time.

With that clarity, a person may not only make better financial decisions, but also feel more confident and more at peace with the direction of their financial life.