Have you ever wondered where your money actually is when you deposit it into a bank? Why banks are able to pay you interest while at the same time lending that same money to someone else? And what would happen if, one day, everyone decided to withdraw their money at the same time?

To understand how banks in the U.S. operate, it is important to look at the history of money, the mechanics of the financial system, and the central role that trust plays in all of it.

The Origin of Banking and Its Role in the Economy

If we look back in history, money has not always existed in the form we use today. In the beginning, people exchanged goods directly with one another—trading fish for salt, or salt for sugar. However, this system quickly became inefficient and difficult to scale for larger transactions.

Over time, people began using valuable assets such as gold as a medium of exchange. But carrying gold was both risky and inconvenient. As a result, individuals started depositing gold in secure places and received paper receipts that could be used for transactions.

This system gradually evolved into paper money, then physical cash, and today into digital money, where most transactions exist only as numbers within electronic systems.

From this evolution, banks emerged as a solution to:

- Store money safely

- Facilitate transactions efficiently

- Support the flow of capital within the economy

Without banks, transactions would be slower, riskier, and significantly more complex.

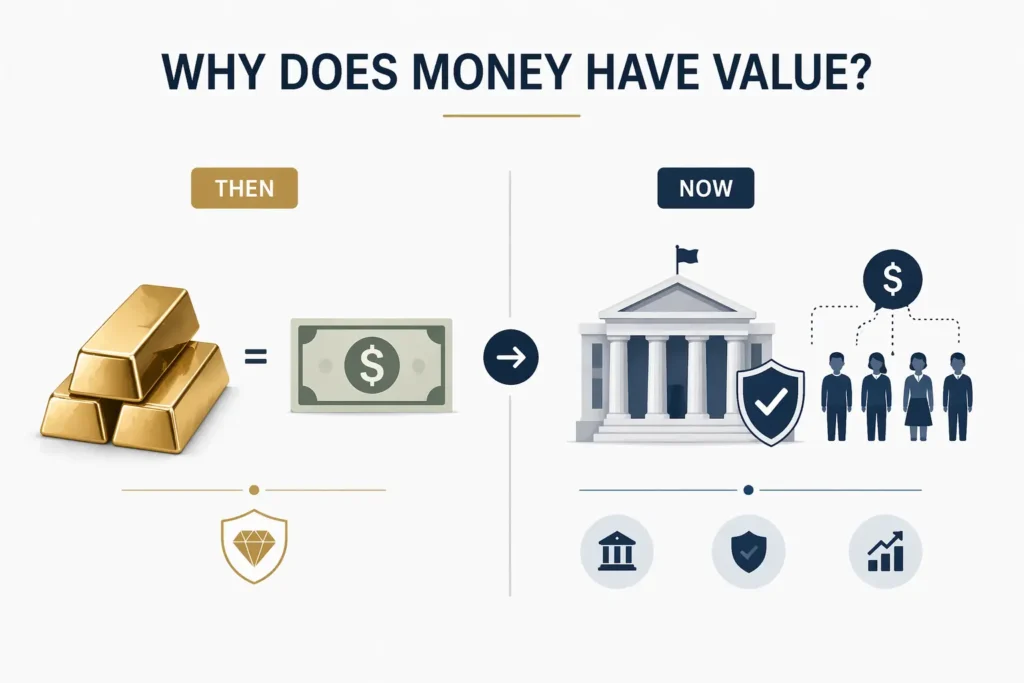

Why Does Money Have Value?

An important question is why money—whether physical or digital—has value.

In the past, money was tied to gold under what is known as the Gold Standard. The value of currency was backed by a tangible asset, and the amount of money in circulation was directly linked to a country’s gold reserves.

Today, however, the U.S. dollar is no longer backed by gold. Instead, its value is based on something more abstract: trust.

This includes:

- Trust in the government

- Trust in the financial system

- Trust in the long-term stability of the economy

This system is referred to as fiat currency, meaning money has value because people collectively accept it and it is recognized as legal tender by the government.

Depositing Money in U.S. Banks and the Role of FDIC

Because the financial system relies on trust, mechanisms are needed to protect that trust. One of the most important institutions in the U.S. banking system is the FDIC (Federal Deposit Insurance Corporation).

The FDIC functions as a form of insurance for bank deposits. Banks pay into the system, similar to how individuals purchase insurance for assets like homes or vehicles.

When you deposit money into an FDIC-insured bank, your funds are protected up to $250,000:

- Per depositor

- Per account type

- Per bank

For example:

- An individual account with $200,000 is fully insured

- A joint account with $450,000 may also be fully insured depending on how ownership is structured

This means that even if a bank fails, deposits within the insured limits are protected. This system plays a critical role in maintaining public confidence when depositing money in U.S. banks.

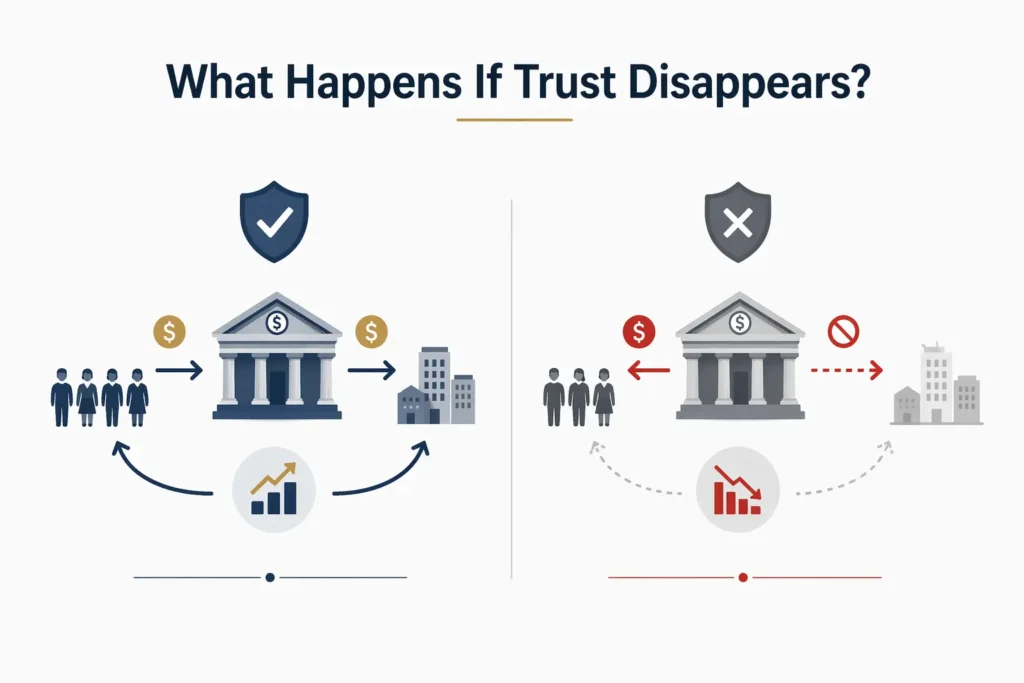

What Happens If Trust Disappears?

If people lose trust in banks and choose to keep cash at home, the consequences extend far beyond individual safety.

Money would stop circulating. It would no longer be used for lending or investment. Businesses would struggle to access capital, and economic growth would slow significantly.

In some countries, this is already a reality. When confidence in the financial system declines, money becomes “frozen,” economic activity weakens, and governments may resort to printing more money—often leading to inflation.

In contrast, when trust is maintained, deposited funds continue to circulate through the banking system, supporting lending, investment, and sustainable economic growth.

How Banks Use Your Deposits

A key concept to understand is that when you deposit money into a U.S. bank, those funds do not simply sit idle.

For example, if someone deposits $100, the bank may retain a portion and lend out the rest. The borrower then spends that money, which is received by others and eventually redeposited into the banking system.

This process repeats multiple times, creating a multiplier effect. From an initial deposit, a much larger amount of money can circulate throughout the economy.

This system works effectively as long as not everyone attempts to withdraw funds at the same time.

Reserve Requirements and Changes Since 2020

Historically, banks were required to hold a certain percentage of deposits as reserves. However, since March 2020, the required reserve ratio in the U.S. has been reduced to 0%.

This means that, legally, banks are not required to hold a fixed portion of deposits as reserves. In practice, however, banks still manage liquidity carefully and must comply with other regulatory requirements to ensure stability.

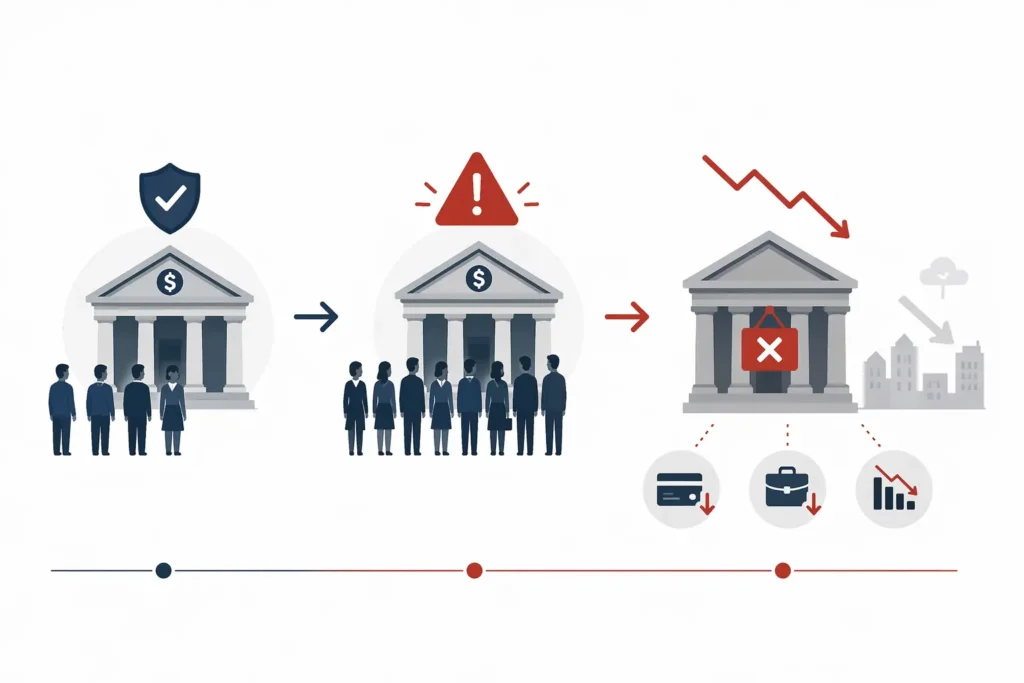

Bank Runs and Systemic Risk

A “bank run” occurs when a large number of people attempt to withdraw their money simultaneously.

The challenge is that banks do not hold all deposits in liquid form, as much of the money has been lent out or invested. When withdrawal demands exceed available liquidity, the bank may face a crisis.

A recent example is Silicon Valley Bank in 2023. As concerns spread, customers—particularly businesses—rushed to withdraw funds. Within days, tens of billions of dollars were requested. The bank was unable to meet these demands and was ultimately shut down.

This illustrates that while the banking system operates smoothly under normal conditions, a loss of trust can quickly lead to instability.

How Banks Generate Profit

Banks are private institutions that operate for profit. When they accept deposits, they do not simply safeguard funds—they use them as a source of capital.

Primary revenue sources include:

- Lending at interest rates higher than what is paid to depositors

- Charging fees for services such as account maintenance, transfers, and card transactions

- Investing in financial assets

From this perspective, deposits are not only a liability for banks but also a key input for generating income.

Conclusion

The entire structure of banks in the U.S. is built upon a single foundational element: trust.

Trust in the value of money, trust in financial institutions, and trust in the system’s ability to function effectively over time.

Understanding how depositing money in U.S. banks works, and how funds circulate within the economy, provides valuable insight into financial decision-making. It allows individuals to better assess risk, manage their finances, and build a stronger long-term financial foundation.