Every time we receive a paycheck, we often see part of our income deducted for Social Security. But not everyone stops to ask: where does that money actually go, how will we receive it later, and when we get older, can we live on Social Security alone?

Many people know that Social Security is a government benefit for retirement, but they may not fully understand how the system works, how they have contributed to it, and how much they may be able to receive in the future. To understand Social Security correctly, it is not enough to only know the definition. It is important to understand the role it plays in the overall retirement plan.

What Is Social Security?

Social Security benefits can be understood as a form of required retirement and financial protection insurance for most workers in the United States. When people work and pay Social Security taxes, they are not simply putting money into a personal account under their own name. They are participating in a broader system designed to support people during some of the most financially vulnerable stages of life.

This system can help support people when they retire, when they become disabled and can no longer work, or when someone passes away and leaves dependents behind. In simple terms, Social Security was created to serve as a basic financial foundation during important life events.

However, it is very important to understand that Social Security was not designed to be the only source of income in retirement. It is only one part of the retirement picture. People may still need additional savings, investments, pensions, retirement accounts, or other assets to maintain a comfortable lifestyle later in life.

If someone relies only on Social Security benefits, their retirement income may be much lower than their current lifestyle requires. People work for many years not just to survive in retirement, but to enjoy life, take care of their families, maintain financial independence, and feel more secure during retirement. For that reason, Social Security should be viewed as a foundation within a retirement plan, not the entire retirement plan.

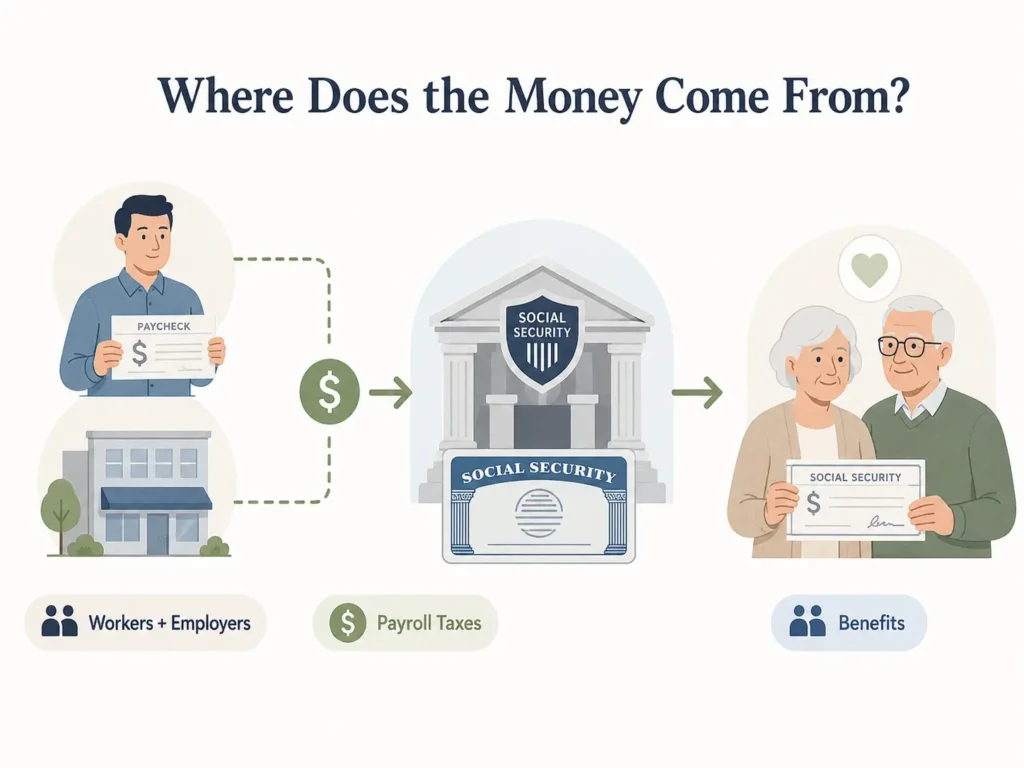

Where Does the Money Come From to Pay Social Security Benefits?

One important part of understanding any financial system is understanding where the money comes from. If money is simply created out of thin air, or if the government just prints more money to pay for everything, that is usually not a sustainable source of funding. When we understand the source of the money, we can better understand whether the system is sustainable and whether it could create other pressures, such as inflation or financial problems in the future.

Social Security is funded mainly through payroll taxes, meaning taxes paid by workers and employers. If you are a W-2 employee, Social Security tax is deducted directly from your paycheck, and your employer also contributes a matching portion. In 2026, the Social Security tax rate is 6.2% for the employee and 6.2% for the employer, applied up to the Social Security taxable wage base of $184,500.

If you are self-employed, meaning you own a business or work independently, you are responsible for both the employee and employer portions. That equals 12.4% for Social Security. In simpler terms, Social Security is not money that naturally appears from the government. It is a system funded by people who are working today to help pay benefits to people who are receiving them today.

Later, when you qualify for Social Security benefits, the next generation of workers will continue contributing to the system to help support your benefits. So Social Security should be understood as a system with money flowing between generations, not as a private savings account that the government keeps separately for each individual.

How Do You Qualify for Social Security Benefits?

Each year, you can earn up to 4 credits toward Social Security. When you work, have income that counts under the Social Security system, and pay the required taxes, you begin accumulating credits.

In 2026, if you earn $1,890 in income that counts toward Social Security, you receive 1 credit. If you earn at least $7,560 in that year, you receive the maximum 4 credits for the year.

To qualify for retirement benefits based on your own work record, you generally need 40 credits, which is equal to about 10 years of work. This is why working, filing taxes correctly, and having your income properly recorded in the Social Security system are important for your future benefits.

How to Check Your Own Social Security Benefits

One of the easiest ways to understand your own benefits is to create your own Social Security account at ssa.gov. Once you log in, you can review your estimated future benefits, your recorded earnings history, your full retirement age, and other important information that applies to your own situation.

In other words, instead of guessing how much you may receive later, you can go directly into the system and see estimates based on your own work and tax record. This is a very basic but important step, because many people talk about Social Security in general terms but have never actually looked at their own record.

The official website to create an account or review your information is: https://www.ssa.gov/myaccount/

When Can You Start Receiving Social Security Benefits?

For Social Security retirement benefits, most people can start receiving benefits at age 62. However, the important thing to understand is that if you claim early, your monthly benefit is usually reduced.

Your full retirement age depends on the year you were born. If you were born in 1960 or later, your full retirement age is 67. If you wait until your full retirement age, you generally receive 100% of your calculated benefit. If you continue delaying after your full retirement age, your monthly benefit can continue increasing until age 70.

So the question is not only when you can receive Social Security, but when receiving it makes the most sense based on your health, income, family situation, and overall retirement plan. Each choice has its own advantages and disadvantages. Some people want to claim Social Security early because they feel they do not know how long they will live, so they want to receive money sooner. Others choose to delay so they can receive a higher monthly benefit in the future, especially if they are healthy, have a family history of longevity, or want to create a larger income source later in life.

For that reason, the answer should be carefully calculated based on each person’s financial situation and retirement goals, instead of following one general rule for everyone.

Who Can Receive Social Security Benefits?

Social Security is not only for the worker. Depending on the situation, a spouse, ex-spouse, children, or surviving family members may also qualify for certain benefits.

For example, if one person worked for many years and has a complete Social Security record, that person’s spouse may qualify for spousal benefits based on the worker’s record. This means that even if the spouse did not work much, or if their own Social Security benefit is lower, they may still be considered for a benefit based on the other spouse’s work record.

If one spouse passes away, the surviving spouse may qualify for survivor benefits. For example, if the husband was receiving a higher Social Security benefit and later passes away, the surviving wife may qualify for survivor benefits based on that higher benefit amount, instead of only receiving the lower benefit based on her own record.

This is why Social Security does not only affect one individual. It can also affect the financial plan of the whole family. However, every situation has specific rules, so instead of guessing, the best approach is to review your own Social Security account or contact the Social Security Administration directly to understand which benefits may apply to your specific situation.

How Much Can You Receive From Social Security?

The amount you receive depends mainly on your lifetime earnings and the age at which you begin claiming benefits. Social Security generally uses your highest 35 years of earnings, adjusted for inflation, to calculate your retirement benefit.

If you worked for fewer than 35 years, the missing years may be counted as zero, which can reduce your benefit. That is why your earnings history matters. In simple terms, the more years you work and the more years you pay Social Security taxes, the greater the opportunity you may have to increase your future benefit.

If you want to know your estimated benefit for your own situation, the best approach is to visit ssa.gov, log in to your account, and review your Social Security statement.

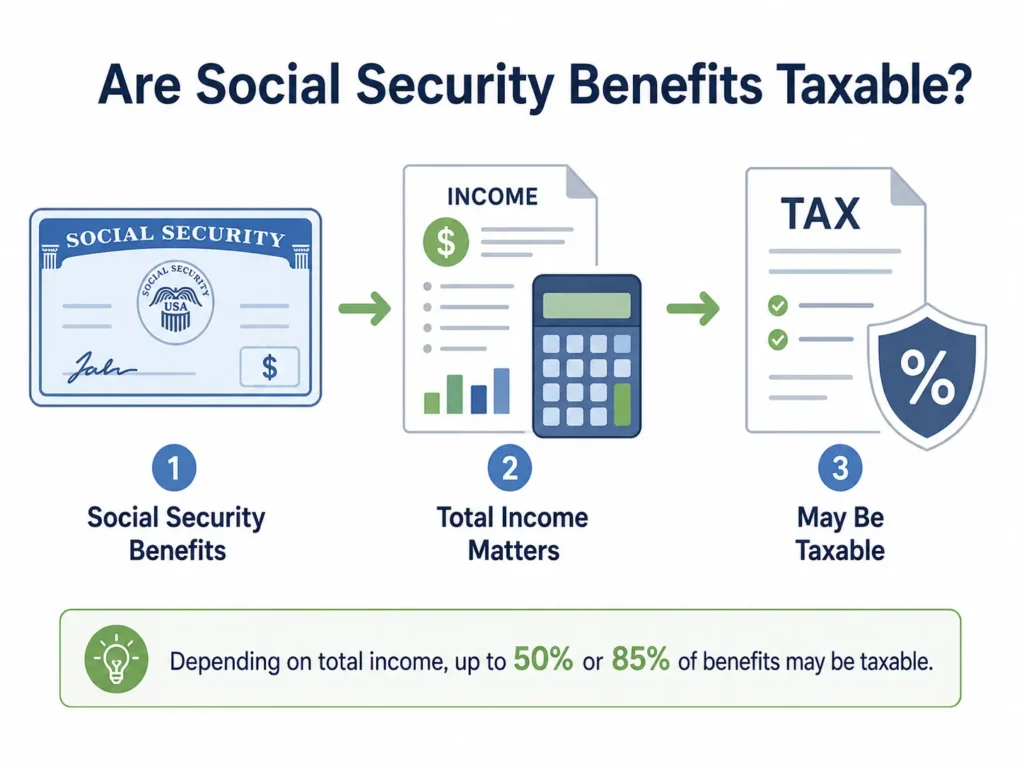

Are Social Security Benefits Taxable?

Social Security benefits may be taxable, but not always. It depends on your total income for the year, including other sources such as wages, withdrawals from certain retirement accounts, investment income, interest income, and part of your Social Security benefit.

If your total income is low enough, only a small portion, or possibly none, of your Social Security benefit may be taxable at the federal level. But if your income is higher, up to 50% or up to 85% of your Social Security benefit may be included in taxable income.

The important thing to understand is that 85% does not mean you pay 85% tax on your Social Security benefit. It means that up to 85% of the benefit you receive may be included in your taxable income. After that, the amount is taxed according to your tax bracket.

Tax planning depends on a person’s full financial picture. There may be ways to reduce taxes in retirement, but that is a separate topic and should be reviewed based on each individual situation.

Does Social Security Protect Against Inflation?

Another important point is that Social Security has some inflation protection. This is one of the reasons Social Security can play an important role in retirement planning.

Social Security benefits can increase over time through cost-of-living adjustments, commonly called COLA. In simple terms, when prices in the economy rise, Social Security has a mechanism to adjust benefits so retirees do not lose too much purchasing power over time.

This matters because during retirement, people may no longer be working and increasing their income the way they did earlier in life, but expenses such as food, housing, insurance, health care, and other living costs may continue to rise. Because of that, COLA helps Social Security become a source of income that can offer more inflation protection than many fixed income sources.

However, even though Social Security has inflation adjustment, it is still only one part of the retirement plan, not the entire retirement plan.

The Main Point to Understand About Social Security

Social Security is an important benefit, so it should not be ignored or underestimated. At the same time, it should not be something people rely on completely. Social Security can serve as a foundation that helps support retirement, disability situations, or family members through survivor benefits when unfortunate events happen.

However, a complete retirement plan should not depend on only one income source. It should be combined with other elements such as savings, investments, retirement accounts, tax planning, insurance planning, estate planning, and other income sources.

When people understand how Social Security works in a simple way, they no longer have to rely only on guessing. They can better understand the role Social Security plays in the overall financial picture and make more informed decisions for their financial future and their family.