Options are one of the financial products often promoted with very attractive claims: turning a few hundred dollars into a few thousand, making money faster than buying stocks, or helping a small account grow quickly. Because of that, options can easily create the impression that they are a shortcut to large profits in the financial markets. But what is often overlooked is that options can also cause investors to lose money very quickly, even when they are partly correct about the direction of a stock.

The issue is not whether options are good or bad. The issue is that many people enter the options market before they truly understand how the product works. A person may know that a call option generally increases in value when a stock rises, or that a put option generally increases in value when a stock falls, but that understanding alone is not enough. Options also involve leverage, premium, strike price, expiration date, intrinsic value, breakeven price, time decay, volatility, bid-ask spread, and very different obligations between the buyer and the seller of the contract.

What Are Options?

Options are a type of derivative. In simple terms, a derivative is a financial product whose value is based on the value of another asset, known as the underlying asset. The underlying asset could be a stock, market index, bond, commodity, or another type of asset.

There are different types of derivatives, including options, futures, forwards, and swaps. Among those, options and futures are two of the most commonly discussed among retail investors. This article focuses on exchange-traded options, which are options contracts traded on organized exchanges.

The popularity of options in recent years has come from several factors. One reason is accessibility. Options have become easier for retail investors to access through brokerage platforms and mobile trading apps. Once a person has a brokerage account and receives options approval, they may be able to buy and sell options contracts directly from their phone. Another reason is social media and financial content built around the idea of getting rich quickly. Many videos and posts highlight large gains made in a short period of time, making options look like an attractive path for a small account to grow quickly.

But the more important question is: how many people truly understand what they are buying? Do they understand the risk inside each options contract? Do they know why an option can lose value even when the stock moves in the direction they expected? Do they understand breakeven price, expiration, or the effect of volatility? Or are many decisions driven mainly by emotion, hope, and stories of big wins seen on social media?

Options are not bad products when they are understood and used properly. Options can be used for hedging, risk management, or building very specific financial strategies. But because options include leverage, expiration dates, sensitivity to price movement, and sensitivity to time, they can cause losses much faster than many people expect when used without a clear understanding of the mechanics.

Options Are Financial Contracts

To understand options, it is important to first understand two basic ideas: option and contract.

An option is a financial contract. In simple terms, it is a legal agreement that connects a buyer and a seller and defines what each side has the right or obligation to do. In everyday conversation, people often say “buying options” or “selling options.” That language is fine casually, but to understand the product more precisely, it is better to think of it as buying an options contract or selling an options contract.

So why is it called an option? Because the buyer of the options contract receives a right, meaning a choice. The buyer may exercise that right, sell the contract to someone else before expiration, or do nothing if the contract is not worth using. The buyer of an option has a right, but not an obligation.

The seller of the option, also known as the person who writes the option, receives the premium from the buyer but takes on an obligation. If the conditions in the contract are met and the buyer exercises the option, the seller may be required to fulfill the obligation written into the contract. This is one of the most important ideas in options: the buyer has a choice, while the seller may have an obligation.

Because exchange-traded options are traded on organized markets, buyers and sellers are not privately writing customized agreements with each other. These contracts are standardized by the market, and transactions take place through brokerage platforms, exchanges, and clearing systems. That structure makes options a formal financial product, but it does not make them simple or risk-free.

Why Leverage Makes Options Attractive

One major reason options are attractive is leverage. In simple terms, leverage means using a smaller amount of capital to control or gain exposure to a larger financial value. This can amplify potential returns, but it can also increase the risk of loss.

In everyday life, people are already familiar with certain forms of leverage, even if they do not always think of it that way. For example, borrowing money to buy a home or a car is a form of leverage. When someone buys a house, they usually do not pay the entire value of the house upfront. They may make a down payment, borrow the rest, and repay the loan over time. In that situation, the house is often used as collateral for the loan. Leverage allows someone to own or control a larger asset than the amount of cash they currently have, but the risk is that if they fail to meet their payment obligations, they may lose the collateral.

In options, leverage does not necessarily come from directly borrowing money. It comes from the structure of the options contract itself. For standard U.S. equity options, one options contract typically represents 100 shares of the underlying stock. That means one contract can provide exposure to the price movement of 100 shares, even though the amount of money paid for the contract may be far lower than the cost of buying 100 shares directly.

For example, suppose Apple stock is trading at $200 per share. Buying 100 shares would cost around $20,000. But buying one Apple call option contract may cost much less, depending on the strike price, expiration date, volatility, and market conditions at that time. This is the appeal of options. With a smaller amount of capital, a person can gain exposure to the price movement of a much larger amount of stock.

At first, this may sound very attractive. A person can spend less money while still benefiting if the stock moves strongly in the expected direction. However, in finance, the important question is always: what is the trade-off?

The trade-off is that options are not the same as owning shares. If someone buys 100 shares of Apple and the stock price drops, they may have an unrealized loss, meaning a paper loss. The value of the position declines, but as long as they still hold the shares, the position does not automatically disappear. A regular stock investment does not have an expiration date.

An options contract is different. Options have an expiration date, meaning the date when the contract expires. If the market does not move in the necessary direction, does not move far enough, or does not move within the time the contract is valid, the contract can lose a large portion of its value or even expire worthless. This means the option expires with no remaining value. Therefore, the fact that options can be cheaper than buying 100 shares directly is not a free advantage. The lower price comes with very different risks.

Call Options and Put Options

There are two main types of options: call options and put options.

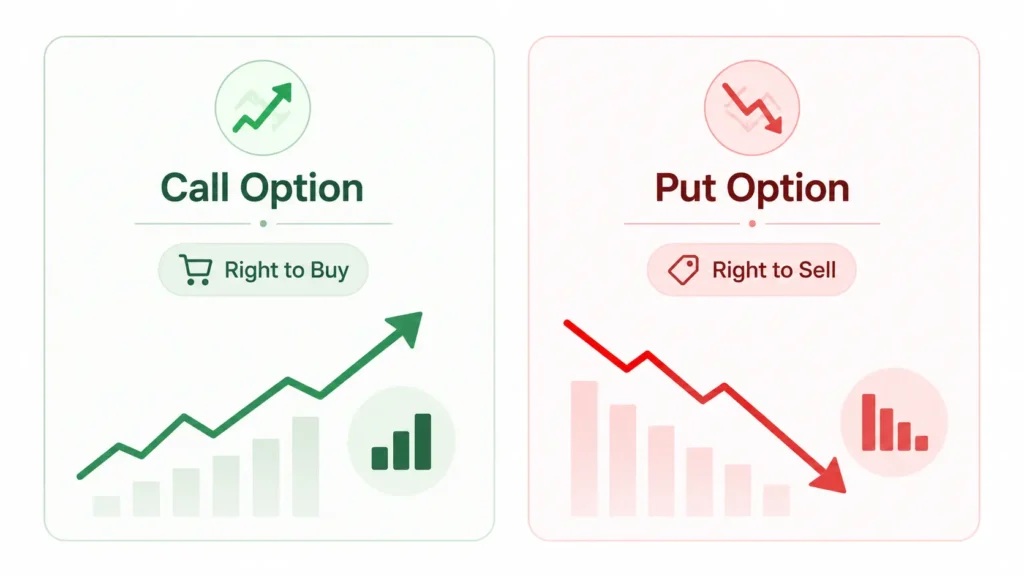

A call option gives the buyer the right to buy the underlying asset at a predetermined price. In simple directional terms, a call option generally becomes more valuable when the underlying asset rises in price, all else being equal.

A put option gives the buyer the right to sell the underlying asset at a predetermined price. In simple directional terms, a put option generally becomes more valuable when the underlying asset falls in price, all else being equal.

With each options contract, there are two basic actions: buy or sell. In trading language, buying is often called going long, while selling is often called going short. Therefore, a long call means buying a call option, a short call means selling a call option, a long put means buying a put option, and a short put means selling a put option.

Another common term is write. Writing an option simply means selling an options contract. The word comes from the idea that the seller is the one creating, or “writing,” the contract that another party buys.

When someone buys an options contract, they must pay a price to own that contract. This price is called the premium. The premium is the amount the option buyer pays to the seller of the contract. For example, if an option is quoted at $2.00, and one standard equity options contract usually represents 100 shares, the total premium paid is usually $200 per contract, before any applicable transaction costs.

This is important because many people see a small number on an options trading screen and assume the contract is very cheap. But option premium is typically quoted per share, while the contract itself usually represents 100 shares. So $2.00 does not usually mean paying $2 total. In most cases, it means paying $200 for one contract.

The easiest way to understand options is to think of them as financial transactions built around a contract. The seller writes the contract. The buyer buys the contract. The buyer pays a premium. In exchange, the buyer receives a right. The seller receives the premium but takes on an obligation to fulfill the terms of the contract if the buyer exercises their right. That is the foundation of options.

Strike Price and Expiration Date

The strike price is the predetermined price written into the options contract. It is the price at which the buyer has the right to buy the underlying asset in the case of a call option, or sell the underlying asset in the case of a put option.

For example, suppose someone buys an Apple call option with a strike price of $200. That means the contract gives the buyer the right to buy Apple stock at $200 per share, regardless of where Apple trades in the market afterward. If Apple rises to $230, the right to buy at $200 becomes more valuable. On the other hand, if someone buys an Apple put option with a strike price of $200, that contract gives the buyer the right to sell Apple stock at $200 per share. If Apple falls to $170, the right to sell at $200 becomes more valuable.

The expiration date is the last day the options contract remains valid. After that date, the contract no longer exists. For example, if an Apple call option has an expiration date of June 19, 2026, the right to buy Apple shares at the strike price written in the contract only remains valid until that date. If the contract expires and the right is not valuable to use, the option may expire with no value.

Unlike stocks, options do not last forever. Time is built directly into the contract from the beginning. This is one of the biggest differences between options and simply owning a stock. With a stock, an investor may sometimes be right over the long term. For example, if someone buys a stock because they believe the company will grow over the next several years, they may continue holding and waiting. But with options, being right over the long term may not be enough. If an investor buys an option that expires in one month, but the stock only moves in the expected direction three months later, the contract may already have expired. In many cases, with options, the investor not only needs to be right about the direction of price movement, but also right before the contract expires.

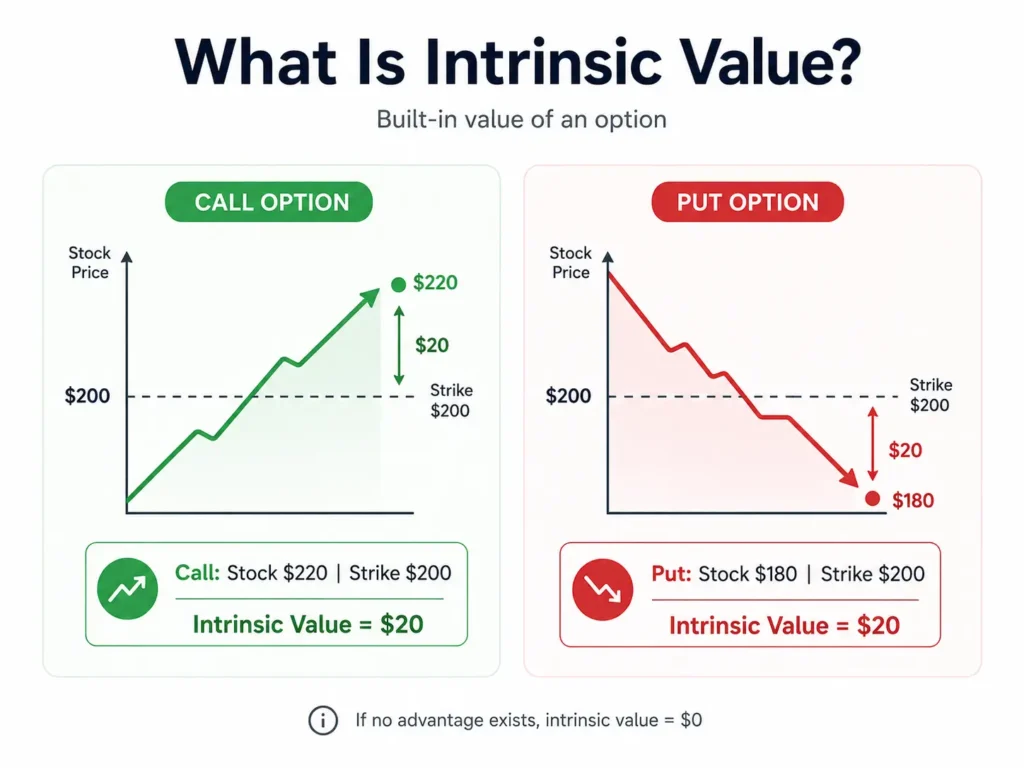

What Is Intrinsic Value?

Intrinsic value is the real value currently inside an options contract at a given moment. More simply, if the option holder used the right in the contract immediately, the benefit from the price difference would be the intrinsic value.

For example, suppose Apple stock is trading in the market at $220, and an Apple call option has a strike price of $200. The contract gives the buyer the right to buy Apple at $200, while everyone else in the market would have to buy it at $220. The $20 benefit from being able to buy below the market price is the intrinsic value of that call option.

But if Apple is trading at only $190 while the call option has a strike price of $200, the right to buy at $200 does not provide any benefit, because Apple can be purchased in the market for less, at $190. In that case, the intrinsic value of the call option is $0. This does not necessarily mean the option has no market price before expiration, but if looking only at intrinsic value, there is no internal value.

For a put option, the logic is reversed. If an Apple put option has a strike price of $200 and Apple is trading at $180, the contract gives the buyer the right to sell Apple at $200, which is $20 higher than the market price. That $20 difference is the intrinsic value of the put option. But if Apple is trading at $210, the right to sell at $200 is not useful because the stock can be sold in the market at a higher price. In that case, the intrinsic value of the put option is also $0.

In the Money and Out of the Money

Two common terms in options are in the money and out of the money. In simple terms, an option is called in the money when it has intrinsic value. That means the right in the contract is beneficial when comparing the strike price to the current market price.

For a call option, the contract is in the money when the current stock price is higher than the strike price. For example, if Apple is trading at $220 and the call option has a strike price of $200, the call option is in the money because the buyer has the right to buy at $200 while the market price is $220.

For a put option, the opposite is true. The contract is in the money when the current stock price is lower than the strike price. For example, if Apple is trading at $180 and the put option has a strike price of $200, the put option is in the money because the buyer has the right to sell at $200 while the market price is only $180.

An option is called out of the money when it does not have intrinsic value. For example, if Apple is trading at $190 but a call option has a strike price of $200, the right to buy at $200 is not useful because Apple can be bought in the market at $190. Therefore, that call option is out of the money. Similarly, if Apple is trading at $210 but a put option has a strike price of $200, the right to sell at $200 is not useful because Apple can be sold in the market at $210. Therefore, that put option is also out of the money.

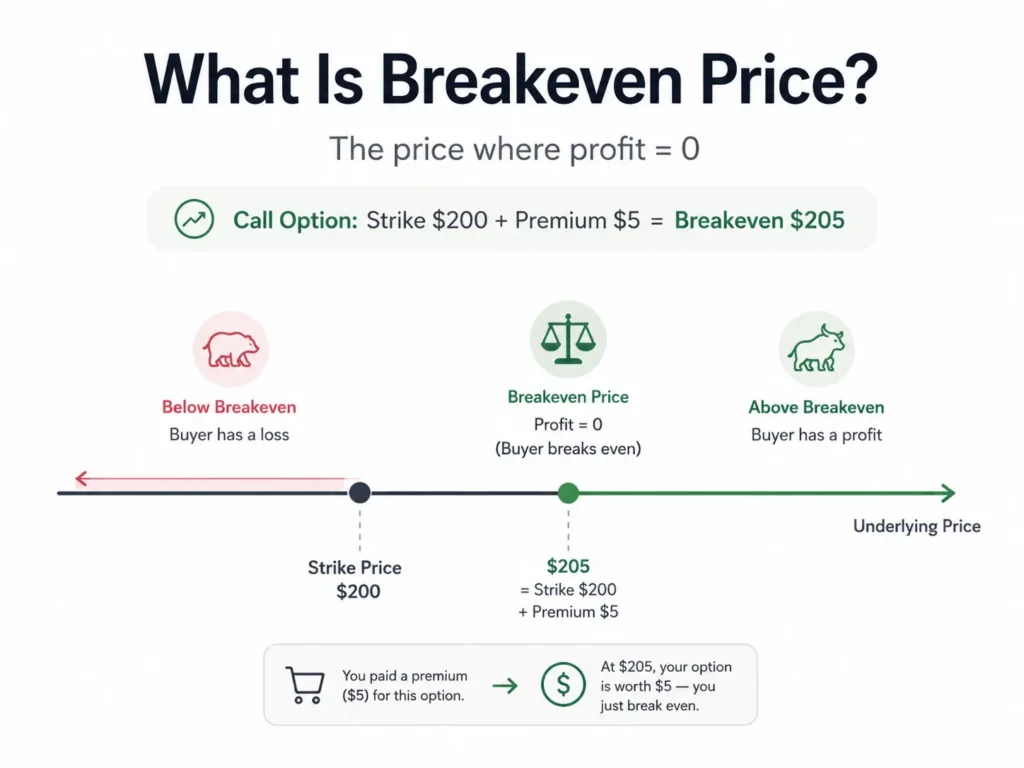

What Is Breakeven Price?

Breakeven price is the price at which, if the option is held until expiration, the buyer recovers the cost paid for the contract. In other words, the position is not profitable, but it is also not losing money. This concept is important because an option being in the money does not necessarily mean the buyer is actually profitable. The reason is that the buyer paid premium upfront.

For example, suppose someone buys an Apple call option with a strike price of $200 and pays a premium of $5 per share. At expiration, Apple does not only need to rise above $200. It needs to rise to $205 for the buyer to reach breakeven. At $205, the contract has $5 of intrinsic value, which is just enough to offset the $5 premium paid. That is the breakeven price. If Apple only rises to $203, the option is still in the money because it has $3 of intrinsic value, but because the buyer paid $5 in premium, the overall position is still losing $2 per share.

For a put option, the calculation goes in the opposite direction. If someone buys a put option with a strike price of $200 and pays a premium of $5, the breakeven price is $195. The stock price must fall below that level at expiration before the position begins generating a net profit, before considering transaction costs and taxes.

Example of a Long Call Option

Suppose a stock is trading at $100. An investor buys a call option with a strike price of $105, expiring in one month, with a premium of $3 per share, or $300 per contract.

This contract gives the buyer the right, but not the obligation, to buy 100 shares of the stock at $105 per share before or at expiration, depending on the type of option. At expiration, if the stock is still below $105, the call option has no intrinsic value, because there is no reason to use the right to buy the stock at $105 when the stock can be purchased in the market for less. If the contract expires out of the money, it may expire worthless, and the buyer loses the entire premium paid.

If the stock rises to $106 by expiration, the option has $1 of intrinsic value. That sounds positive, but the buyer paid $3 for the option. So even though the stock moved in the direction the buyer expected, the position is still losing $2 per share, or $200 per contract, at expiration.

This is a very important point: in options, being right about price direction is not necessarily enough. The price must move far enough, and in many cases fast enough, to overcome the premium paid.

For a long call held to expiration, the breakeven price is calculated as the strike price plus the premium paid. In this example, $105 strike price plus $3 premium equals a $108 breakeven price. That means the stock price needs to be above $108 at expiration for the position to begin generating a net profit, before transaction costs and taxes.

If the stock rises to $115 at expiration, the call option has $10 of intrinsic value. The buyer paid $3, so the net profit is $7 per share, or $700 per contract. This is why people often say buying a call option has limited loss and theoretically unlimited upside. The maximum loss is limited to the premium paid. In this example, the maximum possible loss is $300. The potential profit can be very large if the stock rises significantly. However, this should be stated carefully: the limited loss is clearly defined upfront, while the large potential gain is only a possibility, not a guarantee.

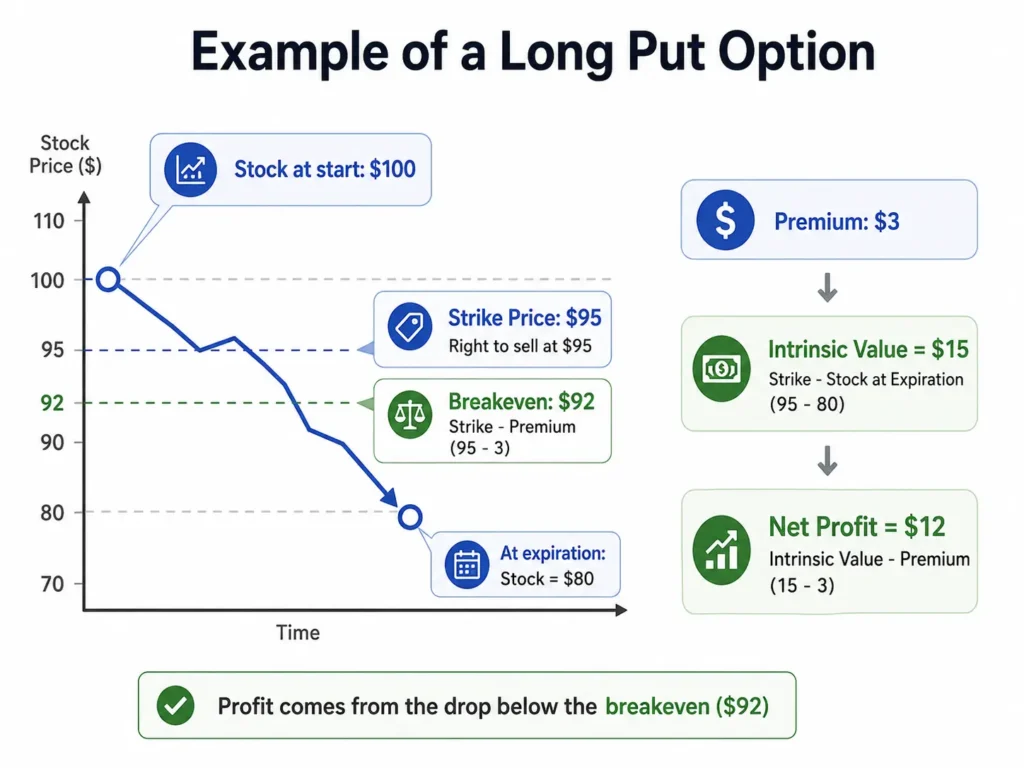

Example of a Long Put Option

A put option works in the opposite direction. Suppose the same stock is trading at $100. An investor buys a put option with a strike price of $95, expiring in one month, with a premium of $3 per share, or $300 per contract.

This put option gives the buyer the right, but not the obligation, to sell 100 shares of the stock at $95 per share. At expiration, if the stock is still above $95, the put option has no intrinsic value, because there is no reason to use the right to sell at $95 when the market price is higher than that. If the contract expires out of the money, it may expire worthless, and the buyer loses the premium paid.

If the stock falls to $94, the put option has $1 of intrinsic value. But the buyer paid $3 for the contract. Once again, even though the stock moved in the direction the buyer expected, the position still has a net loss at expiration.

For a long put held to expiration, the breakeven price is calculated as the strike price minus the premium paid. In this example, $95 strike price minus $3 premium equals a $92 breakeven price. That means the stock price must fall below $92 at expiration for the position to begin generating a net profit, before transaction costs and taxes.

If the stock falls to $80 at expiration, the put option has $15 of intrinsic value. The buyer paid $3, so the net profit is $12 per share, or $1,200 per contract. For a long put, the maximum loss is also limited to the premium paid. The potential profit can be large if the stock falls significantly, but it is not unlimited because a stock price cannot fall below zero.

Risks for Option Sellers

So far, most of the discussion has focused on option buyers. But every option buyer has a seller on the other side of the trade. This is where the risk structure changes significantly.

If someone buys an option, the loss is generally limited to the premium paid. At the time of purchase, the buyer can usually know the maximum amount that can be lost. But if someone sells an option, the maximum gain is usually limited to the premium received, while the potential loss can be much larger depending on the strategy.

For example, if someone sells an uncovered call, also known as a naked call, the maximum profit is only the premium received. But if the stock price rises sharply, the potential loss can be theoretically unlimited, because in theory there is no absolute limit to how high a stock price can rise.

If someone sells a put option, the maximum profit is again limited to the premium received. But if the underlying stock collapses toward zero, the seller can face a very large loss because they may be obligated to buy the stock at the strike price while its market value has fallen far below that level.

This is why selling options does not automatically mean creating “safe income,” even though some people online present it that way. Collecting premium may look consistent for a while, but the obligation behind the trade can become serious when the market moves sharply against the position.

Why Being Right Can Still Lead to Losing Money

One of the most misunderstood parts of options is this: with options, being right about direction is not enough. Many beginners think simply that if a stock will rise, they should buy a call, and if a stock will fall, they should buy a put. That idea is not completely wrong, but it is incomplete.

With an option, at least three things matter. First is direction: will the price go up or down? Second is magnitude: will the price move enough? Third is timing: will the move happen before the option expires?

If an investor is right about direction but wrong about magnitude, the position can lose money. If the investor is right about direction but wrong about timing, the position can also lose money. If the option is purchased at too high a premium, the position can still lose money even if the stock moves roughly as expected. That is why options are much more complex than they may appear at first.

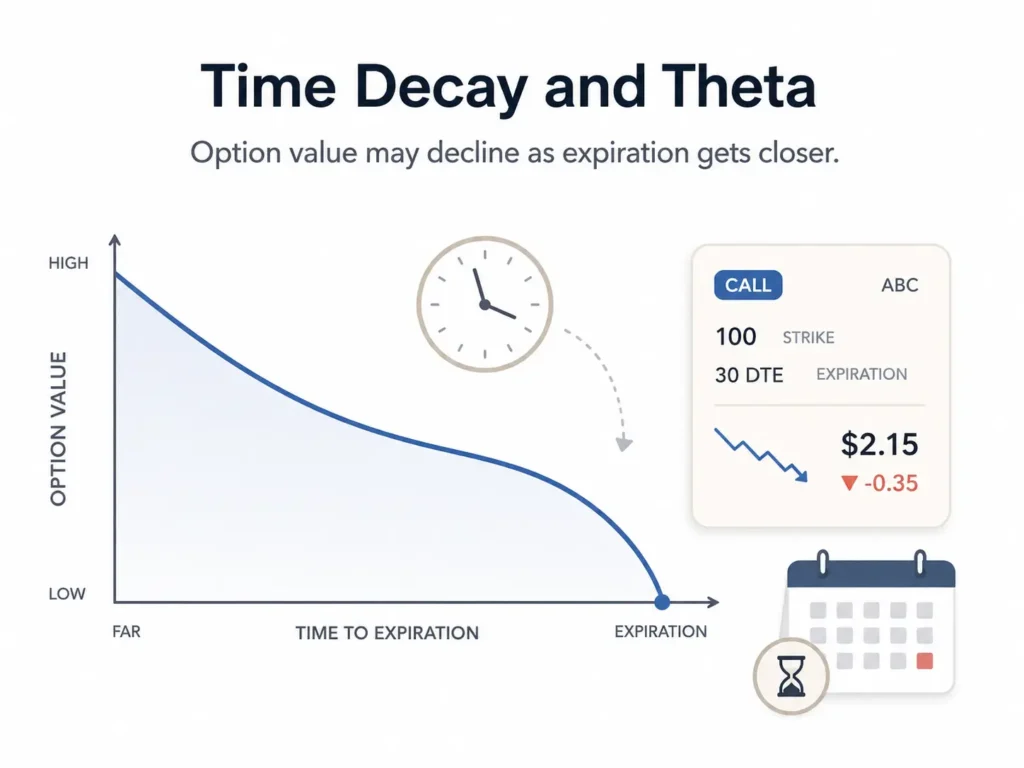

Time Decay and Theta

Another risk many retail investors do not fully understand is time decay, often discussed through the Greek letter Theta.

An option has time value because there is still time for the underlying asset to move in a favorable direction. But as the expiration date gets closer, that time value declines. If all other factors stay the same, an option generally loses value as time passes and expiration approaches. This decay is not always even or linear; in many cases, it can accelerate as the contract gets closer to expiration.

That means for an option buyer, time is often working against them. Imagine someone buys a call option because they believe a stock will rise. The stock does rise a little, but not enough or not quickly enough. Even though the directional view may not be completely wrong, the option can still lose value because time is passing and the contract is approaching expiration.

This is a risk many people do not see when they first start trading options. They focus only on the stock chart. They think that if the stock goes up, their call option should be profitable. But options are not priced only based on the stock price. Time matters. Volatility matters. The premium paid also matters.

Volatility and Implied Volatility

Another important factor is volatility, especially implied volatility. A person does not need to become an options pricing expert to understand the basic idea. When the market expects a stock to make a big move, the options tied to that stock often become more expensive. This commonly happens before events such as earnings announcements.

A beginner may buy a call or a put before earnings because they expect the stock to move sharply. But if that expectation is already reflected in a very expensive premium, the trade becomes much harder to profit from. After the event, implied volatility may drop sharply, and the option price may decline even if the stock moves somewhat in the direction the buyer expected.

This is another reason someone can be “right” and still lose money. They may be right that the stock will move. They may even be right about the direction. But if the premium was too expensive, if volatility drops after the event, or if the move is not large enough, the options trade may still fail to generate a profit.

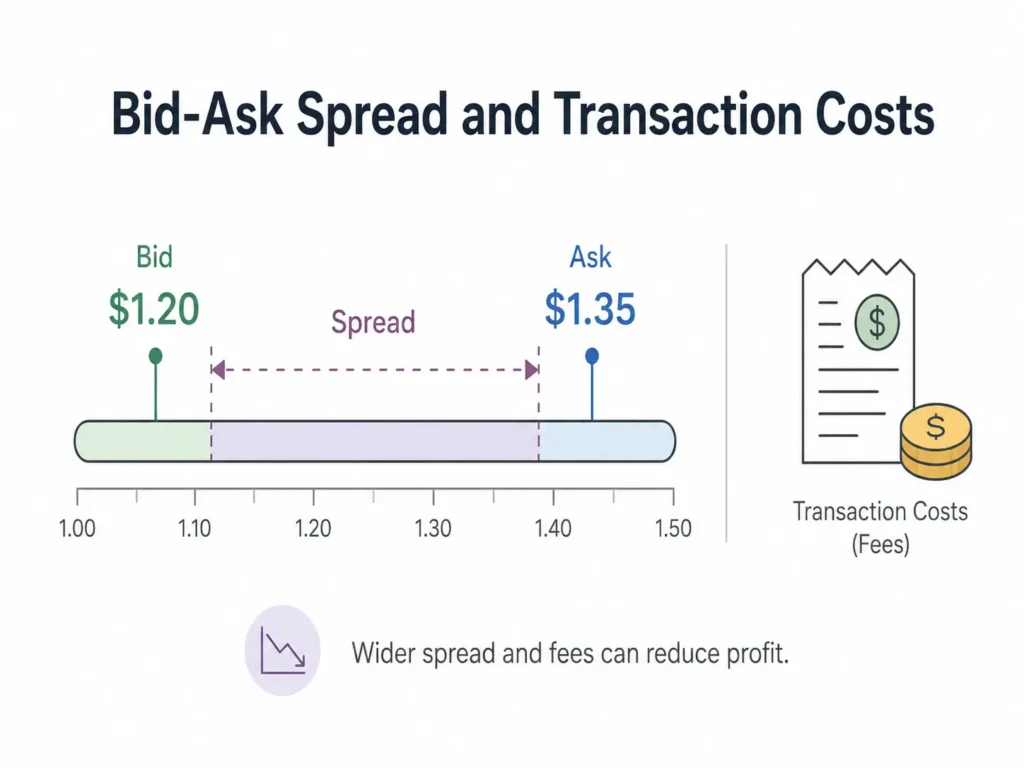

Bid-Ask Spread and Transaction Costs

Another often overlooked factor is the bid-ask spread. The bid-ask spread is the difference between the highest price a buyer is willing to pay and the lowest price a seller is willing to accept for an asset or contract.

In options, the bid-ask spread can become a meaningful cost, especially for contracts with low liquidity, very short expiration dates, or stocks that are receiving heavy market attention. A trader may think they are paying little or no commission, but the real cost can be hidden in the spread between the buying and selling price. The wider the spread, the larger the hurdle the trade must overcome before it can become profitable.

Therefore, evaluating an options trade requires more than just looking at the expected direction of the stock. It also requires understanding premium, time decay, implied volatility, bid-ask spread, liquidity, and all the other factors that can reduce returns or increase risk.

Data on Retail Options Traders

Research on retail options trading presents a sobering picture. A 2023 study published in the Journal of Finance estimated that retail investors lost approximately $2.1 billion trading options from November 2019 to June 2021.

Another study that simulated portfolios based on actual retail options trades found that more than 75% of option trades lost money, and more than half of the simulated options portfolios lost over 90% of their value. Researchers also found that retail investors often overpay for options relative to the volatility that actually occurs later, trade contracts with large bid-ask spreads, and continue holding positions while the contract’s value is eroded over time. In another study on complex multi-leg options strategies, retail investors lost an average of 16.4% over only three days, with losses tending to increase as strategies became more complex.

The point is not that anyone who touches options will automatically lose money. The important point is that the average outcome for retail investors in the options market has historically been very poor, especially when options are used for short-term speculation instead of being structured as carefully calculated risk-management tools.

The Influence of Social Media

One reason many people misjudge the risk of options is social media. People are quick to post a large winning trade. Someone turns $500 into $10,000, and that screenshot spreads everywhere. But very few people post the 20 losing trades that happened before or after that one big win. As a result, viewers see a distorted picture of what options trading actually looks like.

The rare big winner becomes the advertisement. The much more common losses remain almost invisible. This creates a dangerous illusion. Many people begin to believe options are a shortcut to building wealth. But in reality, they may be entering one of the most competitive areas of the financial market, facing professional and sophisticated market participants, while they themselves may not fully understand the risks of the product they are using.

That is why the biggest difference between a professional market participant and an untrained retail trader is not simply intelligence. The more important difference is often preparation, planning, and the ability to calculate risk before making a decision.

A professional usually does not enter a position simply because it “looks like it will go up” or “looks like it will go down.” They usually have a clear framework: what is the risk, what is the potential reward, what needs to happen for the trade to work, what could go wrong, what level of loss is acceptable, what is the exit plan, and how will the position respond if volatility changes, if time passes, or if the market moves against the original expectation?

In other words, they are not only making a prediction. They are building a plan and calculating multiple scenarios in advance. Meanwhile, an individual investor who is not properly prepared may enter the same market with a much weaker process: a feeling, a prediction, a hot stock, a social media video, or the hope of making money quickly.

That is not calculated investing. That is entering a risk the person does not truly understand and then allowing emotion to continue influencing decisions afterward.

Conclusion

Options are not inherently good or bad. They are legitimate financial tools with important use cases. Options can be used for hedging, managing market exposure, or building very specific financial strategies. But at the same time, options are complex. They involve leverage, expiration, time decay, volatility, pricing, and very different obligations between the buyer and seller of an options contract.

If someone does not understand those factors, options can easily become a very expensive lesson. When someone promotes options as a way to use a small amount of money for a very large profit opportunity, they are only telling half the story. The fuller version is that a small amount of money may control a larger market exposure, but that also means losses can happen much faster.

Being right about the direction of price movement does not guarantee that an options trade will be profitable. Time can work against the option buyer. Volatility can work against them. Transaction costs can work against them. Bid-ask spreads can work against them. And research suggests that retail traders, as a group, have historically struggled significantly in this market.

Before participating in a complex financial product like options, the most important thing is not to search for a quick profit opportunity. The most important thing is to understand what the product is, where the risks are, and whether the person truly has enough knowledge to make that decision.

This content is for educational and informational purposes only. It is not a recommendation to buy or sell options, an investment recommendation, or personalized financial advice for any specific situation.

Resources:

Bryzgalova, S., Pavlova, A., & Sikorskaya, T. (2023). Retail trading in options and the rise of the big three wholesalers. The Journal of Finance, 78(6), 3465–3514. https://doi.org/10.1111/jofi.13285

De Silva, T., Smith, K., & So, E. C. (2022). Losing is optional: Retail option trading and earnings announcement volatility. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4050165

Ernst, T., & Spatt, C. (2022). Payment for order flow and asset choice (No. W29883; p. w29883). National Bureau of Economic Research. https://doi.org/10.3386/w29883

Naranjo, A., Nimalendran, M., & Wu, Y. (2023). Betting on elusive returns: Retail trading in complex options. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4404393