Many people hear that a Roth IRA is better because the money can potentially be withdrawn tax-free in the future. Others hear that a Traditional IRA is better because it may help reduce taxes today. So which account is actually better?

The answer is not as simple as saying a Roth IRA is always better or a Traditional IRA is always better. The right choice depends on current income, today’s tax bracket, possible future tax rates, retirement planning needs, and long-term financial goals.

Traditional IRAs and Roth IRAs are both individual retirement accounts within the U.S. financial system. Both can help people save and invest for retirement, but the way they provide tax benefits is very different.

Why Were Traditional IRAs and Roth IRAs Created?

One of the major issues in personal financial planning in the United States is that many people are not financially prepared for retirement. According to an AARP survey, 20% of adults age 50 and older have no retirement savings, and 61% are worried they will not have enough money to support themselves in retirement.

Social Security can be an important part of retirement income, but for many families, Social Security alone may not be enough to maintain the lifestyle they want after they stop working.

Because of this, the U.S. retirement system includes tax-advantaged accounts that encourage individuals to save and invest for their own future. Traditional IRAs and Roth IRAs were both created to help people build retirement assets, alongside other retirement accounts such as 401(k)s.

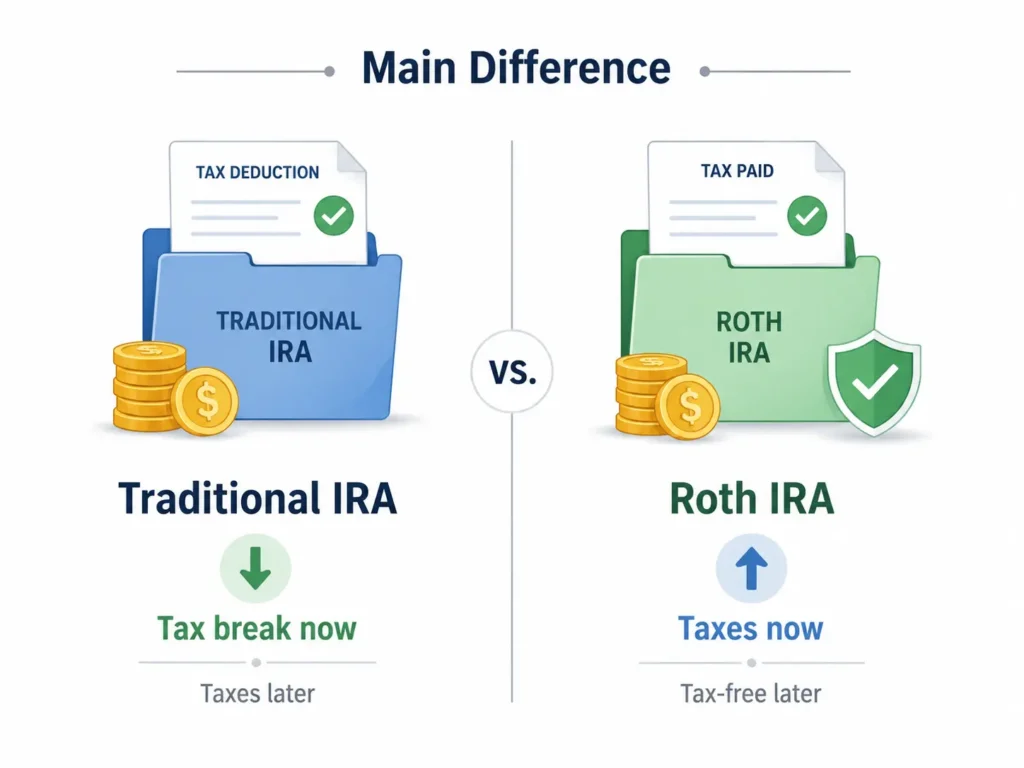

A Traditional IRA provides a tax benefit by potentially reducing taxable income today, allowing the money to grow inside the account, and then taxing the money when it is withdrawn later.

A Roth IRA works in the opposite way. Contributions are made with after-tax money, but if the rules are followed, the growth inside the account may be withdrawn tax-free in the future.

In simple terms, a Traditional IRA is like delaying taxes. A Roth IRA is like paying taxes first in exchange for the possibility of tax-free withdrawals later.

The Main Difference Between a Traditional IRA and a Roth IRA

The biggest difference between a Traditional IRA and a Roth IRA is the timing of taxation.

With a Traditional IRA, contributions may be tax-deductible, but this depends on income, tax filing status, and whether the person is covered by a retirement plan at work. Money inside the account can grow without being taxed each year. However, when money is withdrawn later, the withdrawal is usually treated as ordinary income.

For example, if someone has $70,000 of taxable income in a year and is eligible to contribute $7,000 to a Traditional IRA with a tax deduction, their taxable income may be reduced from $70,000 to $63,000. However, the tax does not disappear completely. It is only delayed until the money is withdrawn in the future.

With a Roth IRA, there is no tax deduction today. The person earns money, pays taxes first, and then contributes after-tax dollars into the Roth IRA. However, if the requirements are met, the growth and future withdrawals may be tax-free.

Another important difference is required minimum distributions, often called RMDs. A Traditional IRA generally requires the account owner to begin withdrawing money at a certain age. A Roth IRA generally does not require RMDs while the original account owner is alive. This creates a major difference in retirement planning and estate planning.

Can Everyone Contribute to a Traditional IRA or Roth IRA?

The short answer is: not completely.

To contribute to an IRA, a person generally needs earned income. Earned income includes wages, salary, or self-employment income. Social Security, investment income, and pension income generally do not count as earned income for IRA contribution purposes.

However, there is an important exception called a Spousal IRA. If one spouse does not work or does not have earned income, but the other spouse does have earned income, the non-working spouse may still be able to contribute to an IRA based on the working spouse’s income in certain situations. This can be useful for households with only one working spouse where both spouses still want to build their own retirement accounts.

With a Traditional IRA, many people with earned income can contribute. However, the more important question is whether the contribution is tax-deductible. Contributing to a Traditional IRA does not always mean receiving a full tax deduction. If the contributor or their spouse is covered by a retirement plan at work, such as a 401(k), the deduction may be limited based on income.

With a Roth IRA, the main issue is the income limit. Not everyone can contribute directly to a Roth IRA. If income exceeds a certain level, the amount that can be contributed directly to a Roth IRA may be reduced or eliminated.

Even if someone has high income, they may still be able to contribute to a Traditional IRA, but the contribution may be non-deductible, meaning it does not reduce taxable income in that year.

How Much Can You Contribute to a Traditional IRA or Roth IRA?

IRA contribution limits can change from year to year, so it is important to check the most current IRS limits.

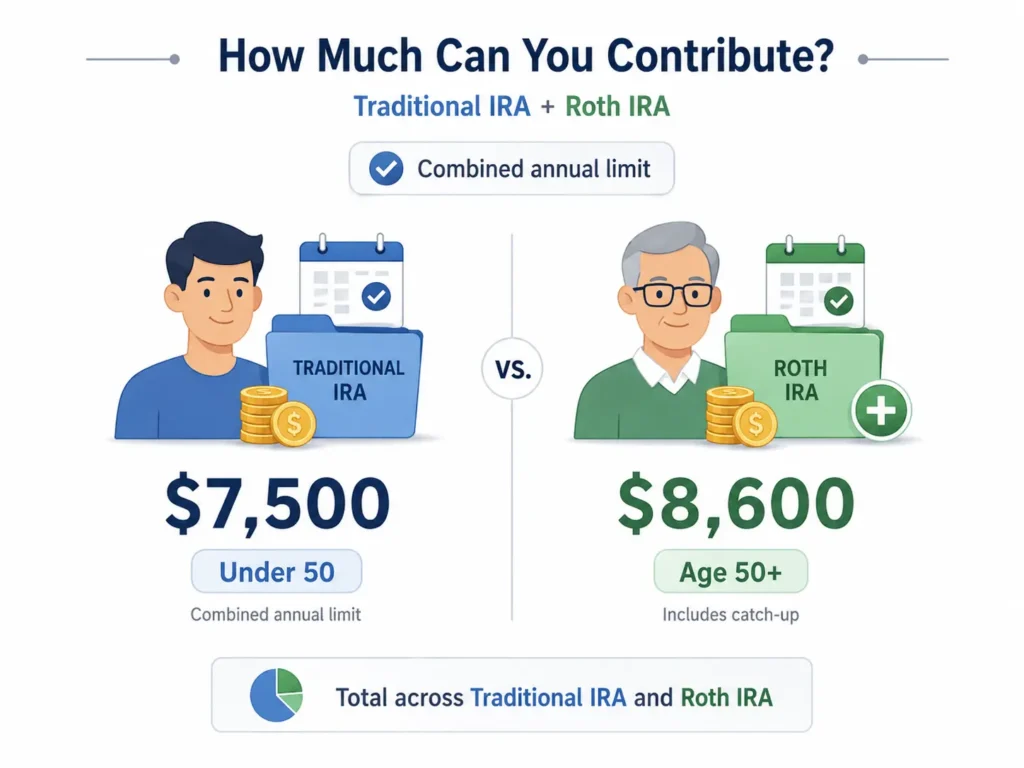

For 2026, a person under age 50 can contribute up to $7,500 to an IRA. A person age 50 or older can contribute up to $8,600 because of the catch-up contribution.

This is the combined limit for all IRAs, not a separate limit for each account. If the limit is $7,500, that does not mean someone can contribute $7,500 to a Traditional IRA and another $7,500 to a Roth IRA. The combined contribution between Traditional IRA and Roth IRA is still $7,500 for someone under age 50.

If a married couple files jointly, each spouse may be able to contribute up to the annual limit to their own IRA, as long as total contributions do not exceed the eligible income of the couple. This may still apply even when only one spouse works, under the Spousal IRA rule.

With a Traditional IRA, high income does not necessarily remove the ability to contribute to the account, but income and workplace retirement plan coverage may affect whether the contribution is tax-deductible.

With a Roth IRA, income limits are more important. In 2026, for someone filing as single or head of household, the ability to contribute directly to a Roth IRA begins to phase out when modified adjusted gross income, or MAGI, reaches $153,000 and may be eliminated at $168,000. For married couples filing jointly, the phase-out range begins at $242,000 and ends at $252,000.

MAGI can be understood simply as the income number the IRS uses to determine whether someone is eligible to contribute directly to a Roth IRA.

What Happens When You Withdraw Money From an IRA?

This is an important area because many people focus on contributing money but do not think enough about what happens when money is withdrawn.

With a Traditional IRA, if the money contributed in the past was deducted from taxable income, withdrawals are generally taxed as ordinary income. For example, if someone later withdraws $20,000 from a Traditional IRA, that amount may be added to their taxable income for the year. The tax owed depends on their tax bracket at the time of withdrawal.

If money is withdrawn too early, before age 59½, the withdrawal may also be subject to an additional 10% penalty unless an exception applies. Some exceptions may include qualified medical expenses, qualified education expenses, a first-time home purchase within certain limits, disability, or a distribution after the account owner’s death. However, these exceptions usually help avoid the 10% penalty, not necessarily income taxes if the withdrawal is still taxable income.

With a Roth IRA, withdrawals are more complicated but may also be more flexible in some situations. Money directly contributed to a Roth IRA is after-tax money. Because of this, the contribution portion, meaning the money already contributed and already taxed, can often be withdrawn without tax or penalty.

However, the earnings, meaning the growth or investment gains inside the account, must meet certain requirements to be withdrawn tax-free. In general, to withdraw Roth IRA earnings tax-free, the account must satisfy the 5-year rule, meaning the Roth IRA must have been open for at least five years, and the person withdrawing generally needs to be at least age 59½. Other qualifying situations may include disability, death, or a first-time home purchase within certain limits.

The key point is that it matters whether the withdrawal is coming from contributions or earnings, when the withdrawal happens, and whether the withdrawal meets IRS rules.

What Is a Required Minimum Distribution?

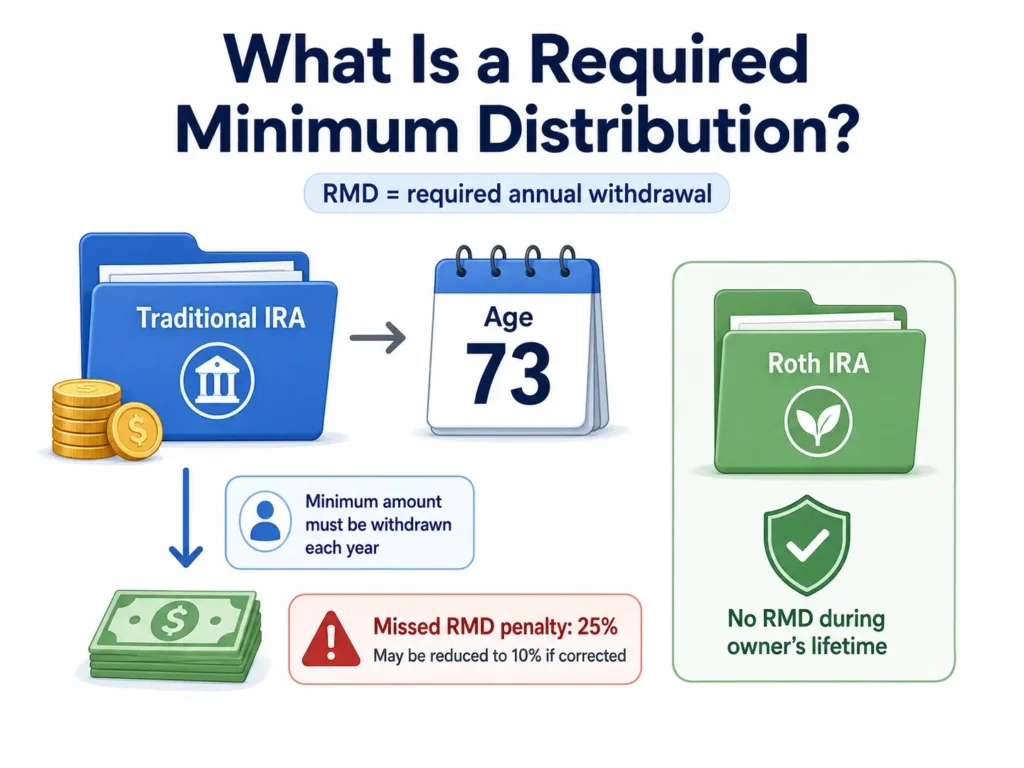

A required minimum distribution, often called an RMD, is the minimum amount the government requires someone to withdraw from certain retirement accounts once they reach a certain age.

With a Traditional IRA, the account owner cannot leave the money in the account forever without withdrawing it. Because the government allowed taxes to be deferred for many years, the IRS eventually requires withdrawals to begin. When the money is withdrawn, it generally creates taxable income.

For many people today, required minimum distributions generally begin at age 73.

This matters because required withdrawals can affect taxes during retirement. If someone has a large Traditional IRA, the required annual withdrawal may also be large. That withdrawal can increase taxable income, push the person into a higher tax bracket, affect Medicare premiums, or reduce tax planning flexibility.

If the required minimum distribution is not taken on time, the amount not withdrawn may be subject to a 25% penalty. If the mistake is corrected in a timely manner within two years, the penalty may be reduced to 10%.

This is one reason people should not only think, “Reducing taxes today is always good.” Reducing taxes today can be helpful, but if the Traditional IRA becomes very large later and required withdrawals increase taxable income in retirement, planning should begin early.

In contrast, a Roth IRA does not have required minimum distributions while the original account owner is alive. This gives Roth IRA more flexibility in retirement planning and estate planning.

What Can You Invest In Inside an IRA?

One common misunderstanding is thinking that an IRA is an investment. An IRA is not an investment. It is a type of account.

An IRA can be viewed as a tax-advantaged container. Inside that container, the account owner may choose different investments or financial products, depending on where the account is opened and the rules of the custodian, which is the company or institution that holds and manages the investment account.

Inside an IRA, many people may invest in mutual funds, ETFs, stocks, bonds, money market funds, or other investment products.

The important point is that risk and return do not come from the name IRA. Risk and return come from the investments held inside the IRA.

If the investment portfolio is too risky compared to the investor’s risk tolerance, the IRA can still lose value. If the portfolio is too conservative while the investor is still young, the account may not grow enough to support retirement goals in the future.

So the question is not only whether to open a Traditional IRA or Roth IRA. The next question is what investment strategy should be used inside the account.

The account is only the tax structure. The investment strategy inside the account is what determines whether it aligns with the investor’s goals, time horizon, and risk tolerance.

Is Roth IRA or Traditional IRA Better?

This may be the most important question. Many people like Roth IRA because it sounds very attractive: pay taxes today, let the money grow, and potentially withdraw it tax-free later. That is a powerful benefit.

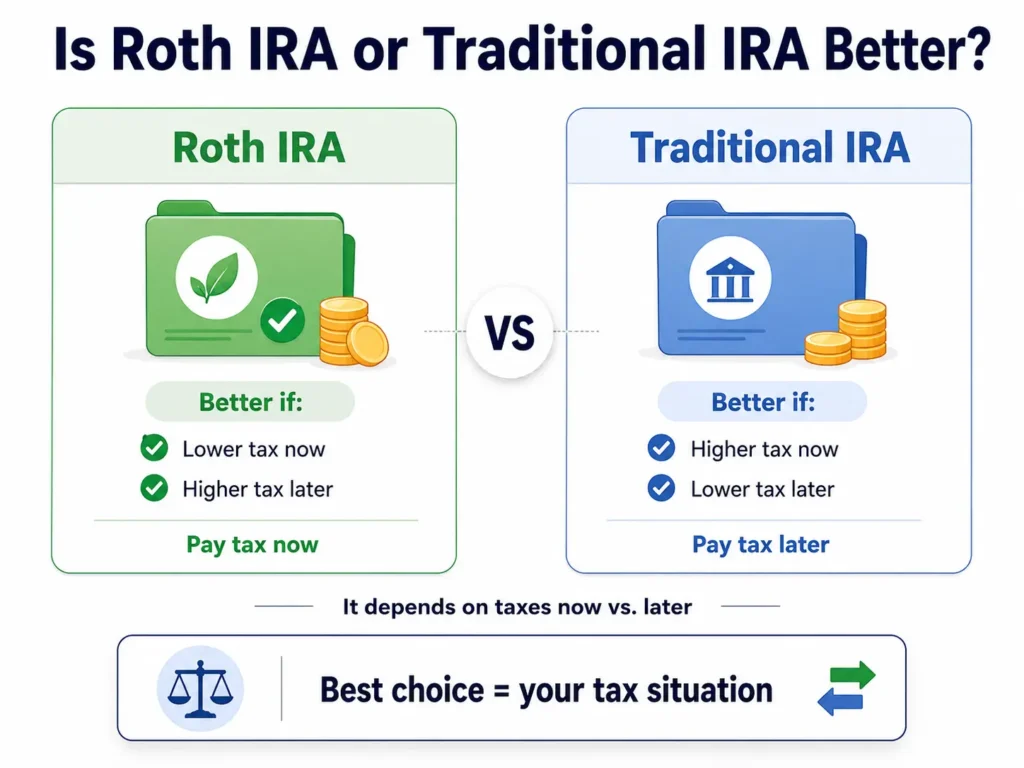

But saying Roth IRA is always better than Traditional IRA is not accurate. A better way to think about it is to ask: are taxes today higher or lower than taxes may be in the future when the money is withdrawn?

If someone is in a low tax bracket today and expects to be in a higher tax bracket later, a Roth IRA may make sense. That person pays taxes while the tax rate is lower and may have the ability to withdraw money tax-free later. For example, a young worker with lower income and many years for the money to grow may find a Roth IRA attractive.

But if someone is in a high tax bracket today and expects taxable income to be lower in retirement, a Traditional IRA may be more beneficial. The reason is that the person may receive a tax deduction at a higher rate today and later withdraw the money when the tax rate may be lower.

The important point is that Roth IRA and Traditional IRA are not absolutely good or bad. They differ mainly in when taxes are paid. If tax rates today and tax rates in the future are the same, the after-tax result may be mathematically similar. But in real life, taxes do not stay still. Income changes, tax laws change, family situations change, careers change, and retirement plans change.

Because of this, the best strategy is not always 100% Roth IRA or 100% Traditional IRA. In many cases, having both may create better flexibility. This is called tax diversification.

Just as investment planning often involves diversifying assets, retirement planning may also involve diversifying account types: taxable accounts, tax-deferred accounts, and tax-free accounts. That flexibility can be very important in retirement.

What Happens to an IRA When the Account Owner Dies?

This is a topic many people do not like to think about, but it is very important, especially for those who have family, children, or a desire to leave assets to the next generation.

When the account owner passes away, the IRA can be transferred to the beneficiary listed on the account. The beneficiary designation is very important and can have a major impact. Depending on the situation, the person listed as the IRA beneficiary may matter more than what is written in a will.

Because of this, it is important to review IRA beneficiaries regularly, especially after major life events such as marriage, divorce, having children, the death of a family member, or changes in estate planning goals.

With a Traditional IRA, the beneficiary will generally have to pay taxes when money is withdrawn because the account has not been fully taxed before.

With a Roth IRA, if the account meets the requirements, the beneficiary may receive better tax treatment because Roth IRA withdrawals may be tax-free in many situations. However, inherited IRAs still have their own rules about when money must be withdrawn.

Under the SECURE Act, many non-spouse beneficiaries, meaning beneficiaries who are not the spouse of the original account owner, generally must withdraw the inherited IRA within 10 years, although certain exceptions may apply.

This means an IRA is not only a retirement planning tool. It can also be part of estate planning, or the plan for transferring assets to family members or beneficiaries.

When thinking about an IRA, the question should not only be: how much tax does this account save this year? Another important question is: how will this account affect retirement income, future taxes, and the assets left to family?

Summary

Traditional IRAs and Roth IRAs are both important tools in personal financial planning in the United States. A Traditional IRA may help reduce taxes today, allow money to grow tax-deferred, and then create taxable income when withdrawals are made later. A Roth IRA does not reduce taxes today, but if the rules are followed, it may allow tax-free withdrawals in the future and create more flexibility in retirement planning.

There is no universal answer for everyone. A Roth IRA is not always better than a Traditional IRA. A Traditional IRA is not always better than a Roth IRA.

The real questions are: how might taxes today compare with taxes in the future? Is reducing taxes now more important, or is tax-free flexibility later more valuable? Does the account fit the broader plan for retirement, investing, taxes, and the assets intended for family or beneficiaries?

When these questions are understood, IRA planning becomes less confusing. It becomes a tool that helps investors and retirement savers make more informed decisions about their financial future.

This content is for educational purposes only and should not be considered investment, tax, legal, or personalized financial advice. Before making a decision, individuals should consult the appropriate professional based on their specific situation.