Cash can feel safe. It is simple, familiar, easy to access, and easy to understand. For many people, having cash available creates a sense of control. It feels more stable than the stock market, less complicated than investment accounts, and more private than the financial system.

But from a personal finance perspective, the real question is not just whether cash makes someone feel safe. The more important question is whether that cash is actually helping build wealth, prepare for retirement, protect the family, and create better opportunities for the future.

Cash has an important role in a financial plan. Everyone needs some level of liquid savings for everyday expenses, emergencies, and short-term goals. The problem begins when cash becomes too large of a portion of someone’s overall financial life. Holding too much cash for too long can create hidden costs, including theft risk, limited insurance protection, lack of financial history, missed investment growth, and a weaker retirement plan.

Why do people like holding cash?

People hold cash for many reasons. Some do it because of habit. Some do it because they have had negative experiences with banks, investments, debt, taxes, paperwork, or the financial system. Others simply feel more comfortable seeing and controlling their money directly.

Emotionally, that is understandable. Cash can feel more certain than a number on a bank statement or investment account. It does not fluctuate from day to day the way the market does. It can also feel more private and easier to use.

However, the feeling of safety is not always the same as true financial safety. If someone holds too much cash for many years, that money may create emotional comfort, but financially, it may not be doing much. It does not grow. It does not compound. It does not build financial history. It does not create retirement income. And over time, it may not keep up with the rising cost of living.

The better question is not whether cash is good or bad. The better question is: how much cash should be held, for how long, and for what purpose?

Is cash at home really safe?

Keeping cash at home can feel convenient because the money is available at any time. If someone keeps a few hundred or a few thousand dollars at home for emergencies, that may be reasonable. But when the amount becomes much larger, such as tens of thousands of dollars or more, the risk increases significantly.

Cash at home can be stolen during a break-in. It can be destroyed in a fire, damaged by water, lost during a move, misplaced, or accidentally thrown away by someone who does not know what it is. Another major issue is proof. If someone says they had $30,000, $50,000, or $100,000 in cash at home, how would they prove that after the money is gone?

Many people assume homeowners insurance or renters insurance will fully cover stolen cash. In reality, coverage is usually limited. According to GEICO, renters insurance may cover stolen cash, but the coverage limit is often very low, sometimes only around $200 to $300, because cash is difficult to verify after it is lost or stolen: https://www.geico.com/information/aboutinsurance/renters/does-renters-insurance-cover-stolen-cash/

This means someone may feel in control because the money is physically in the house. But if that money disappears, the chance of recovering it may be very limited. Cash at home may feel private and accessible, but it is not necessarily protected the way many people assume.

Does a safe deposit box protect cash?

Another option people consider is placing cash in a safe deposit box at a bank. Compared to keeping cash at home, a safe deposit box may sound safer. In some cases, it can be useful for storing important documents, jewelry, property records, birth certificates, or items that are difficult to replace.

However, a safe deposit box is not the same as a bank account. When money is deposited into an eligible bank account at an FDIC-insured bank, that money may be protected up to applicable FDIC limits. But the contents inside a safe deposit box are different.

According to the FDIC, the contents of a safe deposit box are not insured by the FDIC. Financial institutions generally do not insure the contents of safe deposit boxes either. In simple terms, the bank is renting out storage space. It is not treating the items inside the box as deposits in a bank account: https://www.fdic.gov/consumer-resource-center/five-things-know-about-safe-deposit-boxes-home-safes-and-your-valuables

Safe deposit boxes also create access issues. They usually can only be opened during bank hours. If there is an emergency after hours, on a weekend, after the box owner passes away, or if family members do not have the proper legal documents, accessing the box can become complicated. A safe deposit box can be a storage tool, but it should not be confused with a financial strategy.

The real cost of holding too much cash

One of the biggest costs of holding too much cash is opportunity cost. This cost is often invisible because no one sends a bill showing how much growth was missed. But over time, the difference between invested money and idle cash can become significant.

For example, assume two people have similar financial situations. Each person has $20,000 per year available to save or invest. Person A invests the full $20,000 each year. Person B invests $10,000 each year and keeps the other $10,000 in cash.

Now assume the investment earns an average annual return of 7%. This is only a hypothetical example to illustrate compound growth. It is not a promise of return, not a projection of future performance, and not a recommendation for any specific investment. Actual markets fluctuate, and investing always involves risk.

After 20 years, Person A could have about $820,000 in the investment account. Person B could have about $410,000 invested, plus $200,000 in cash, for a total of about $610,000. The difference is about $210,000.

After 30 years, Person A could have about $1.89 million. Person B could have about $945,000 invested, plus $300,000 in cash, for a total of about $1.24 million. The difference is about $645,000.

The lesson is simple: cash does not disappear, but it also does not grow. Invested money has the opportunity to compound year after year. Holding too much cash can be expensive, even when that cost does not appear as a monthly fee.

When cash has no clear financial history

In personal finance, having money and being able to use money clearly are not the same thing. When money stays outside the financial system, it can become harder to explain, harder to verify, and harder to use when it is actually needed.

If someone wants to buy a home, apply for a mortgage, borrow money for a business, prove assets, plan for retirement, transfer assets to children, work with a financial professional, or create an estate plan, documentation matters. Financial institutions often need to know where the money came from, how long it has been held, and whether it can be verified.

The same issue can happen within a family. If cash is stored at home and the only person who knows where it is becomes sick, passes away, or can no longer manage the finances, the family may not know how much cash exists, where it is located, or how it should be handled.

A clear financial history is not just paperwork. It connects money to a plan. It helps prove ownership, organize taxes, support retirement planning, and make it easier to transfer assets clearly to the next generation.

Cash and retirement planning

Cash can feel safe while someone is still working because income continues to come in. But in retirement, the question changes. It is no longer just “How much money do I have?” The more important question becomes: “How long can this money last?”

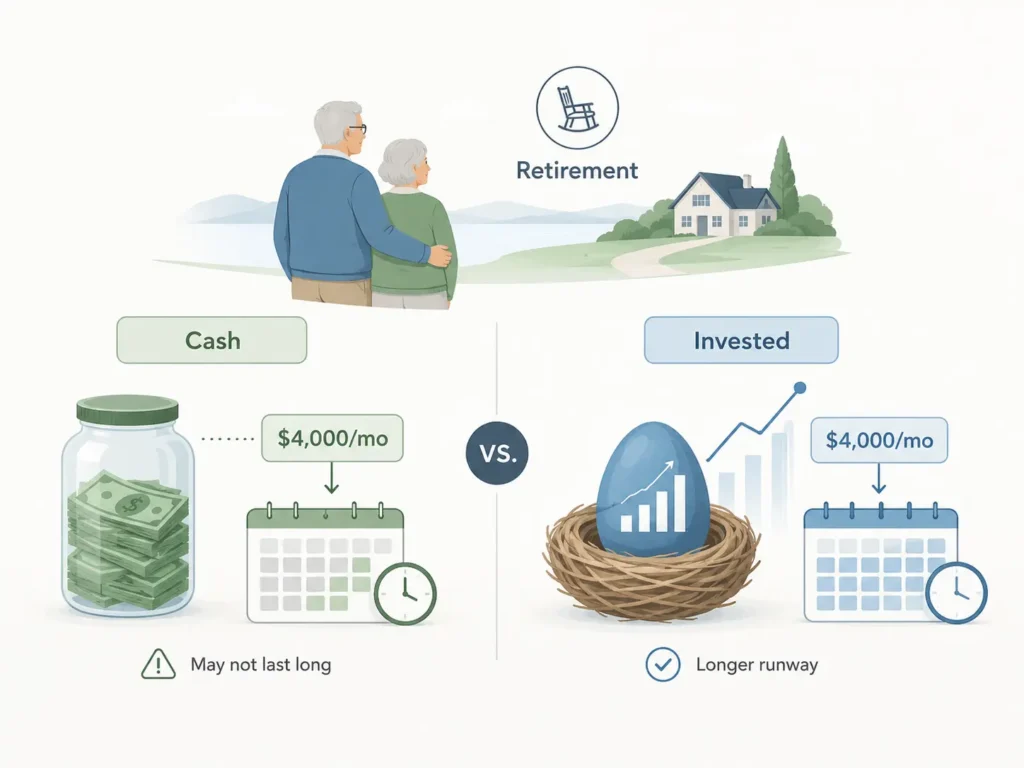

For example, if someone saves $10,000 per year in cash for 30 years, they will have $300,000. That may sound like a large amount. But if they need $4,000 per month in retirement, that $300,000 would last about 75 months, or a little over six years. This does not include inflation, healthcare costs, emergencies, or long-term care expenses.

Now compare that with another person who also saves $10,000 per year but invests it consistently for 30 years. Using the same hypothetical 7% average annual return, that money could grow to about $945,000. If this person withdraws $4,000 per month in retirement, even with no additional growth, the money could last almost 20 years. If the account continues to earn a hypothetical 4% average annual return during retirement, the calculation suggests it could last close to 39 years.

This is still only an illustration. Real markets do not move in a straight line, returns are not guaranteed, and taxes, fees, withdrawal timing, and investment risk can all affect the outcome. But the example shows an important point: when cash is spent, the balance simply goes down. When money is invested and managed appropriately, it may still have the opportunity to work during retirement.

Financial aid, benefits, and long-term planning

Financial aid, healthcare assistance, housing support, and other government or institutional benefits can be very important during difficult periods. Each program has its own rules, and those rules may depend on income, assets, household size, state, age, health status, immigration status, and other factors. This article is not legal, tax, or benefits advice.

From a personal finance perspective, the broader question is whether someone should build their entire financial life around keeping assets unclear or outside the system.

Support programs may help during certain stages of life. But if a person’s long-term financial strategy is mainly based on “not showing assets,” that approach can limit future opportunities. It may reduce investment growth, make retirement planning harder, complicate home buying or borrowing, weaken financial documentation, and make it more difficult to transfer assets to the next generation.

Benefits can be part of a temporary support system, but they should not become the entire financial strategy for life.

The real role of cash in personal finance

Cash is not bad. In fact, cash is necessary when it is used for the right purpose. Everyone should have some liquid money for everyday expenses, emergencies, short-term goals, and peace of mind.

The issue is not whether someone should have cash. The issue is how much cash, for how long, and for what purpose. If the money is needed soon, cash may be appropriate. But if the money is meant for retirement, long-term wealth building, or leaving assets to the next generation, keeping it in cash forever may not be the best use of that money.

Instead of asking, “Should I hold cash or invest?” a better question is, “What job does each dollar have?” Cash can protect short-term life needs, while investing can help build long-term financial security.

Conclusion

Holding cash can create a sense of safety, but financial safety is not only about being able to physically hold money. It is also about whether the money is protected, documented, growing, and connected to a clear financial plan.

Cash has an important role, but cash should not be the entire financial plan. If the goal is to build wealth, prepare for retirement, and create a stronger future, money usually needs a clearer structure within the financial system so it has the opportunity to grow over time.

Disclaimer: This article is for general financial education only. It is not investment, tax, legal, insurance, or personalized financial advice. Examples are hypothetical and do not guarantee future investment results. Investing involves risk, including the possible loss of principal.