IUL, or Indexed Universal Life insurance, is often presented as a very attractive financial tool. At first glance, it may sound like one product can do almost everything: provide market-linked growth, protect against market downturns, create tax-free income, and provide life insurance protection for the family.

Because of that, IUL is often promoted as a solution for many different financial needs. Need to invest? Buy IUL. Need life insurance? Buy IUL. Need to prepare for a child’s college education? Buy IUL. Want to leave money for the next generation? Buy IUL. Want to prepare for retirement? Also buy IUL.

The issue is not that IUL is always bad. In certain situations, IUL may have a role in a financial plan, especially when the buyer truly needs permanent life insurance and has the ability to maintain the policy over the long term. The bigger issue is how the product is sometimes explained. When important details are left out, buyers may think they are purchasing a simple investment, when in reality they are signing a long-term life insurance contract with costs, rules, limitations, and a fairly complex structure.

What Is IUL?

IUL stands for Indexed Universal Life insurance. It is a form of permanent life insurance.

To understand IUL, it helps to first understand the difference between term life insurance and permanent life insurance. Term life insurance provides coverage for a specific period, such as 10, 20, or 30 years. The buyer pays premiums to receive protection during that period. If something unfortunate happens while the policy is active, the insurance company pays a death benefit to the family. If the term ends and nothing happens, the coverage usually ends.

Permanent life insurance is different. This category includes whole life, universal life, and indexed universal life. These policies are generally designed to last longer, and many of them include a cash value component inside the policy.

IUL is a type of permanent life insurance that provides both life insurance protection and cash value. The cash value may be credited interest based on a formula connected to a market index, such as the S&P 500. But that does not mean the buyer’s money is directly invested in the S&P 500. This is a very important distinction because many misconceptions begin here. When people hear “linked to the market,” they may think they are investing in the stock market. In reality, they own a life insurance contract with its own rules, costs, limits, and interest-crediting formula set by the insurance company.

What Is a 7702 Strategy?

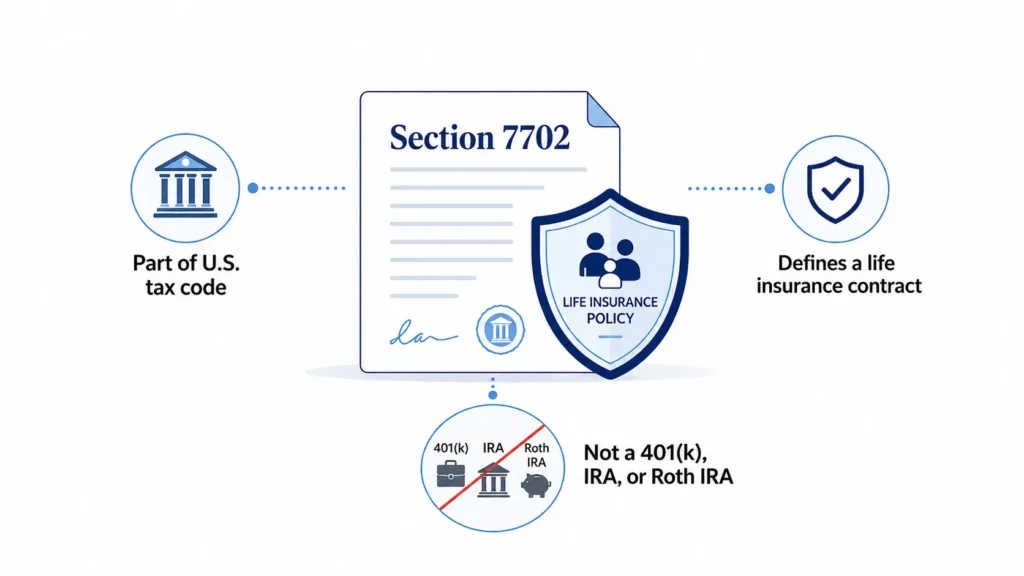

Some people today do not call the product IUL. Instead, they may call it a “7702 strategy,” “7702 plan,” or “retirement tax code 7702.” That wording can make the product sound newer, more professional, and more like a special tax strategy.

However, 7702 is not a separate investment account. It is also not a retirement account like a 401(k), IRA, or Roth IRA. Section 7702 of the U.S. tax code is used to define when a contract qualifies as a life insurance contract for federal tax purposes.

In simple terms, when someone says “7702 strategy,” in many cases they are still referring to a cash value life insurance policy, such as whole life, universal life, or IUL. So if a product is introduced as a “7702 plan” instead of IUL, the buyer should ask clearly: What is the actual product? Is it a life insurance policy? Does it have cash value? Does it have surrender charges? Does it have internal insurance costs? And if the product is essentially IUL, why not call it IUL directly?

Source: U.S. Code, Title 26, Section 7702 — Life insurance contract defined: https://www.govinfo.gov/content/pkg/USCODE-2024-title26/pdf/USCODE-2024-title26-subtitleF-chap79-sec7702.pdf

Why Is IUL Promoted So Heavily?

One reason IUL is promoted so heavily is because the sales story sounds very attractive. A buyer may hear that their money can grow with the market, be protected when the market goes down, be accessed tax-free later, and still provide life insurance protection for the family if something unexpected happens.

For many people, that sounds almost too good to ignore. IUL may be presented as a product that can solve multiple problems at once: investing, retirement, taxes, college funding, life insurance, and wealth transfer.

Another reason is the commission structure. Many life insurance products are sold through a commission-based model, meaning the salesperson may be paid when the policy is issued. This does not mean commissions are always bad. But buyers should understand that the person recommending the product may be compensated when the contract is sold. In particular, permanent life insurance policies with cash value, such as IUL, often have higher premiums than simple term life insurance, which means commissions may also be significantly higher.

Source: NerdWallet — Life insurance agent commissions: https://www.nerdwallet.com/insurance/life/learn/life-insurance-agent-commissions

Does IUL Give Market Growth Without Market Risk?

One of the most common claims about IUL is that buyers can receive stock-market-linked growth without taking stock market risk. That sounds attractive, but it is only part of the picture.

The key point is that an IUL policy may be linked to a market index such as the S&P 500, but the buyer’s money is usually not directly invested in the S&P 500. Instead, the insurance company uses a formula to determine how much interest is credited to the policy. This is often called a crediting method.

That formula may include several limits. A cap rate is the maximum interest rate the policy can receive during a crediting period. A participation rate determines how much of the index gain is used in the calculation. A spread is an amount deducted before interest is credited.

For example, if the S&P 500 rises 10% in one year, that does not mean the cash value inside an IUL policy will rise 10%. Depending on the policy formula, after applying the cap rate, participation rate, spread, or other limits, the credited interest may be 8%, 7%, 6%, or another number.

In addition, when the buyer does not directly own stocks or index funds, they do not receive all the benefits of being an actual investor, such as direct ownership, reinvested dividends, account transparency, liquidity and trading flexibility, or full participation when the market performs strongly.

If the Market Goes Down, Does IUL Really Lose Nothing?

Another common sales point is that when the market goes down, the buyer does not lose anything. This usually relates to the idea of a 0% floor.

If the market drops 10% in a year, an insurance salesperson may say that with IUL, the buyer does not lose money because the floor is 0%. This can feel comforting, especially for people who are afraid of market risk. But the important detail is that the 0% floor usually refers to the interest-crediting rate, not necessarily the total policy value after all costs.

Even in a year when the policy is credited 0%, the contract may still deduct insurance costs, administrative fees, rider charges, and other internal expenses. A simple way to think about this is homeownership. If the value of a house does not drop this year, the owner still has to pay property taxes, homeowners insurance, repairs, maintenance, and utilities. The fact that the house value did not decline does not mean there were no costs.

This is also important when comparing IUL with investing. In investing, market risk is part of the price an investor accepts for the opportunity to earn higher long-term returns. If a product reduces or removes market risk, there is usually a trade-off somewhere else, such as limited upside, insurance costs, surrender charges, or contract complexity.

Is an IUL Illustration a Guarantee?

The policy illustration is one of the most misunderstood parts of IUL. On paper, the cash value may appear to grow every year, and the projected values at retirement age may look very attractive.

But an illustration is not a guarantee. It is a projection based on assumptions. Looking at an IUL illustration is similar to looking at a map before a long road trip. The map may say the trip takes six hours, but that assumes no traffic, no accidents, no road closures, no bad weather, and no long stops. The actual trip may be very different.

An IUL illustration works the same way. It depends on assumptions about credited interest, policy costs, premium payments, and how the buyer may use policy loans in the future. If the buyer only looks at the most attractive projected column, they may think that result is almost certain to happen. In reality, it is important to review the guaranteed values, policy charges, surrender charges, loan assumptions, and lower-crediting scenarios.

Can IUL Average 7% or More?

Another potentially misleading statement is that IUL can average 7% or more. This may cause buyers to believe they will receive 7% every year, or that 7% is the real return after all costs.

But IUL does not work that simply. A 6%, 7%, or higher number is often an illustrated rate, not the actual net return to the policy owner.

Think about someone earning $100,000 per year. That number may sound very good, but it is income before taxes, housing, transportation, food, insurance, family expenses, and other costs. After all those expenses, the amount actually left for saving or investing may be only $20,000 or $30,000, not $100,000.

IUL is similar. The illustrated rate is not the same as the net return after all policy costs and limitations. The actual return depends on policy charges, insurance costs, cap rates, participation rates, spreads, surrender charges, loan interest, and how the policy is funded over time. If an insurance company could truly guarantee 7% or more every year after all expenses, it would be one of the most powerful financial products in the world.

Source: Colva Insurance Services — Intro to IUL analysis: https://www.colvaservices.com/intro-iul/

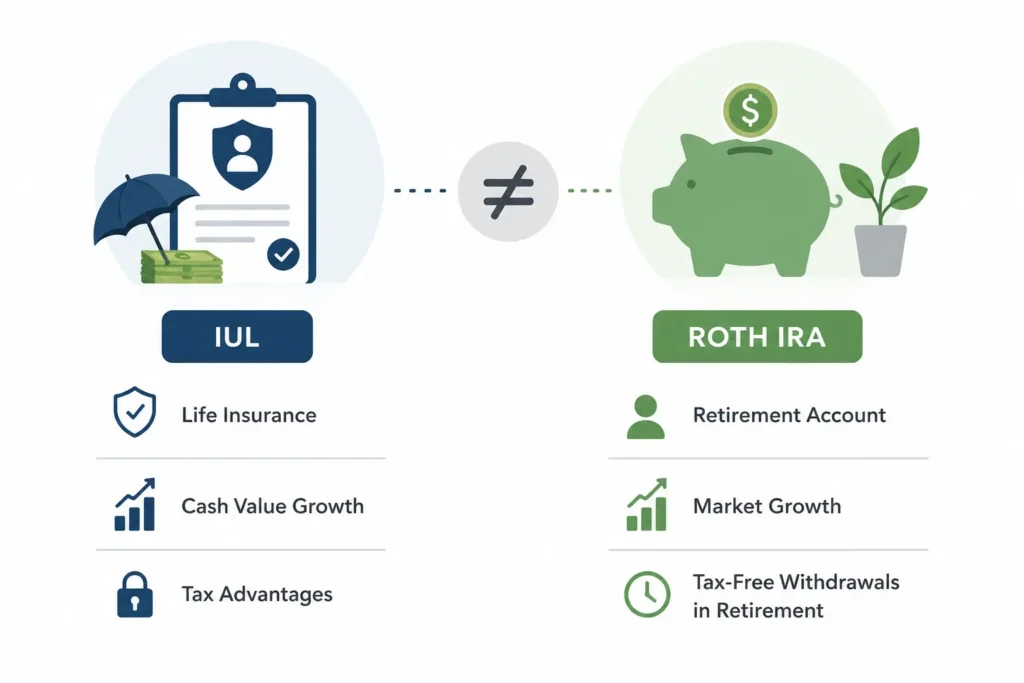

Is IUL Like a Roth IRA, but Better?

Another common comparison is that IUL is like opening a Roth IRA, but better. This can lead buyers to think that if IUL is that good, they may not need a Roth IRA, Traditional IRA, or 401(k). They may think buying IUL is enough.

But a Roth IRA and IUL are not the same type of account. A Roth IRA is a retirement investment account. Its main purpose is to help someone invest for the future under a specific set of tax rules. IUL is different. Its original purpose is still life insurance. The cash value is a feature inside the insurance contract, not a reason to treat it like a Roth IRA.

Both Roth IRA and IUL may have tax advantages, but tax advantages do not make them the same tool. One is primarily designed for retirement investing. The other is primarily designed to provide life insurance protection, with a cash value component added inside the contract.

Is Money From IUL Really Tax-Free?

Another common statement is that buyers can access money from IUL whenever they want without paying taxes. This may make buyers feel that their money is still there and can be used whenever needed.

This can be true in certain situations, but the explanation is often oversimplified. Many people hear “tax-free income” and imagine withdrawing money from a savings account. But with IUL, money is often accessed through a loan against the cash value of the policy.

If the policy is properly designed and managed, the loan may not be taxable at the time it is taken. But it is still a loan. And because it is a loan, it may have loan interest. It may reduce the cash value, reduce the death benefit, and if the loan accumulates over many years, it can affect the long-term ability to keep the policy in force.

In a worse scenario, if the policy lapses, money that the buyer previously thought was “tax-free” may create a large tax problem later. So if the explanation only focuses on the tax-free part but leaves out policy loans, loan interest, policy costs, and lapse risk, the buyer is only hearing half of the story.

Banks and Wealthy People Use IUL. Should Everyone Else Buy It Too?

Another persuasive sales point is that banks and wealthy people use IUL, so regular families should also buy it. But not every strategy used by wealthy families is appropriate for everyone. Circumstances, goals, risk tolerance, budget, family responsibility, and tax situation can be completely different.

Banks, corporations, and wealthy families may use life insurance for very specific purposes, such as estate planning, executive benefits, liquidity planning, tax strategy, or legacy planning. They may also have attorneys, tax professionals, accountants, and financial advisors reviewing complex strategies before using them.

A regular family may not have the same needs, budget, or support team to manage that product over the long term. A strategy can be legitimate in one situation and inappropriate in another.

Should IUL Replace a Complete Financial Plan?

A product with many features does not automatically become a good financial plan. Some people may say IUL is better than an investment account or retirement account because it includes growth, protection, tax benefits, and life insurance in one product. That sounds attractive, but combining many features into one product does not automatically make the product better.

IUL should not be sold as a magical financial product that can replace investing, retirement planning, college planning, tax planning, and estate planning all at the same time. The important questions are where the benefits come from, what the costs are, what trade-offs the buyer is accepting, and whether the product truly fits that person’s situation.

For many people, insurance should be used to protect the family against financial risk, while investing should be used to build long-term wealth. These two goals can support each other within a broader financial plan, but they should not be mixed together so much that the buyer no longer understands what they are buying or what they are giving up.

The goal is not to avoid life insurance. The goal is to understand what is being purchased, why it is being purchased, what it costs, and what role it plays in the long-term financial plan.

Disclaimer: This content is for general financial education only. It is not investment, tax, legal, insurance advice, or a recommendation to buy or sell any specific financial product. Every individual and family has a different financial situation. Before making decisions related to life insurance, investing, taxes, or retirement planning, consider consulting qualified professionals who understand your specific circumstances.